SC — INSIGHTN°47

SoundInsightN°45

01

Q1 earnings season provides fundamental confirmation of the AI investment cycle.

02

Monetary policy is becoming more challenging as growth and inflation keep rates elevated.

03

Power, grids and financing are emerging as the key bottlenecks of the next phase.

Bonds

Overview

Interest Rates

Credit Spreads

UnattractiveAttractive

Equities

Overview

Equity Risk Premium

Leading Indicators

Risk Index

UnattractiveAttractive

Posted 5/26/2026 by Christian Luchsinger

AI Boom: The Numbers Do the Talking

In the last edition of SoundInsights, we argued that markets are becoming increasingly better at distinguishing between short-term media noise and the structural signal embedded in fundamentals. Four weeks later, this assessment can be refined: the signal has not only strengthened—it is beginning to show up visibly in macroeconomic data.

The first-quarter 2026 reporting season reveals an economic momentum that few would have expected to this extent only a few months ago. At the same time, a notable shift has taken place in bond markets: yields are rising, expectations for rate cuts are fading, and monetary policy is, for the first time in quite a while, moving from being a tailwind to a potential headwind.

These two developments are more closely connected than they may appear at first glance. The AI boom is no longer merely an equity-market narrative. It is now visible in earnings, investment budgets, order backlogs, electricity demand—and increasingly also in interest-rate markets.

An Unusually Strong Earnings Season

Around 90% of S&P 500 companies have reported their results for the first quarter of 2026. Of these, 83% exceeded earnings expectations—well above the five-year average of 78%. Aggregate earnings growth is likely to come in at around 29%. That would make it the strongest quarter since late 2021 and the sixth consecutive quarter of double-digit earnings growth.

The outlook also remains robust. For full-year 2026, analysts currently expect earnings growth of around 22%. Particularly noteworthy is that estimates have been revised higher since the start of the reporting season. Normally, the opposite tends to happen during an ongoing earnings season.

For investors, this is crucial. Rising share prices can always be driven by sentiment, liquidity or short-term exuberance. Rising earnings, by contrast, are the fundamental foundation of a sustainable market cycle. This is precisely the foundation that the current earnings season is providing.

AI: Investments Are Turning into Cash Flows

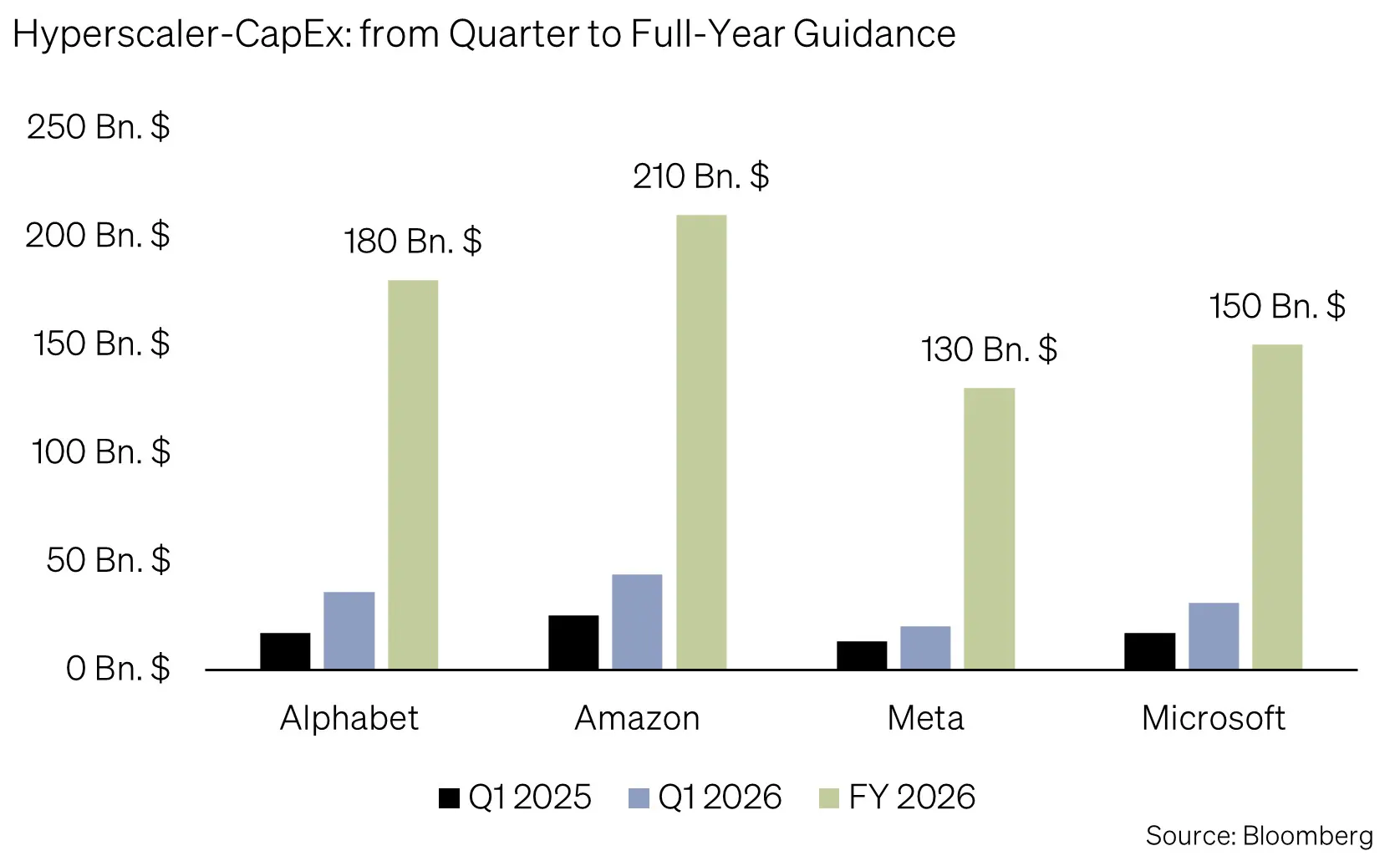

Artificial intelligence remains the most visible growth driver. The major technology companies continue to invest at a pace that is historically exceptional.

Capital expenditure by the leading hyperscalers has almost doubled year on year:

- Alphabet: USD 36 billion, up from USD 17 billion a year earlier

- Microsoft: USD 31 billion, up from USD 17 billion

- Amazon: USD 44 billion, up from USD 25 billion

- Meta: USD 20 billion, up from USD 13 billion

Three of the four major providers have once again raised their full-year investment guidance. In total, CapEx spending of around USD 725 billion is expected for 2026—almost twice as much as in the previous year. Including Oracle and CoreWeave, Bloomberg Intelligence estimates the figure at more than USD 820 billion.

Even more important is the demand side. Google Cloud’s order backlog nearly doubled within a single quarter, rising from USD 240 billion to more than USD 460 billion. CEO Sundar Pichai openly stated that the company is currently “compute-constrained.” Put differently: demand is there. Capital is there. What is missing is capacity.

For private investors, this is a central message. The AI cycle is no longer driven primarily by expectations. It is increasingly showing up in real revenues, real orders and real investment.

NVIDIA Shows Just How Strong Demand Really Is

Anyone seeking to verify whether the investment plans of the major technology companies have real substance should look at the supplier side. There, NVIDIA remains the most important barometer.

In the quarter ending in April, NVIDIA generated revenue of USD 81.6 billion—85% more than a year earlier. For the current quarter, management is guiding for USD 91 billion, around USD 4 billion above market expectations. Gross margin stands at roughly 75%, while the free-cash-flow margin is just under 50%. Such figures are exceptional even within the technology sector.

Particularly telling are the contractual purchase commitments. These rose from USD 95 billion to USD 145 billion in just three months. These are not non-binding statements of intent, but balance-sheet-relevant purchase obligations for future deliveries.

The hyperscalers are therefore not only buying for current demand. They are reserving capacity for years to come. Bank of America estimates the addressable market for AI infrastructure at around USD 3 trillion by 2030—roughly four times today’s level.

When the Digital Wave Reaches the Real Economy

Perhaps the most important point is this: the AI boom is not confined to the technology sector. It is increasingly becoming a driver of real economic growth.

The Bank for International Settlements shows that IT-related investment in the United States now accounts for around 5% of GDP—more than during the dot-com bubble in 2000. The key difference from that period, however, is crucial: around the turn of the millennium, it was mainly user companies investing in internet infrastructure. Today, the producers themselves are investing—the companies that build, operate and monetise the digital infrastructure.

That makes today’s cycle more capital-intensive, but also more fundamentally grounded.

An analysis by BCA Research concludes that AI-related investment explains around half of US GDP growth. Harvard economist Jason Furman put it even more clearly: investment in information processing and software may account for only around 4% of GDP, but it was responsible for a disproportionately large share of growth in the first half of 2025.

This makes clear what is structural about the current earnings season: the AI investment cycle has now become one of the most important growth drivers of the world’s largest economy.

Interest Rates: From Tailwind to Headwind

Bond markets have not remained unaffected by this development. The yield on 10-year US Treasuries recently rose above 4.65%—the highest level since January 2025. Thirty-year yields climbed back above 5%, while two-year yields moved above 4% for the first time in eleven months.

At the same time, interest-rate expectations have shifted significantly. Only a few weeks ago, markets were still pricing in further rate cuts. Now, even the possibility of a rate hike this year is once again being seriously discussed. The US Federal Reserve left its policy rate unchanged at 3.5–3.75% at the end of April, but four dissenting votes within the Fed committee show how contentious the situation has become.

The key is to interpret this correctly. Rising yields are often reflexively equated with inflation concerns. Yet a significant part of the current move likely reflects not only inflation, but also stronger growth. When companies invest heavily and demand productive capital, real yields rise. This is a different kind of interest-rate increase than the one seen in 2022 and 2023.

Back then, the focus was on the inflation shock and monetary tightening. Today, part of the rise in rates stems from stronger investment demand. For risk assets, that is considerably more constructive—but it changes the valuation framework.

The era of extremely low interest rates that defined the decade after the financial crisis is over. Investors should prepare for higher rates to be more than just a temporary phenomenon.

Power Is Becoming the Critical Bottleneck

Alongside capital and chips, another factor is coming to the fore: electricity.

Microsoft reports an order backlog of around USD 80 billion for Azure capacity that currently cannot be served. The reason is not a lack of hardware, but insufficient power supply. Estimates suggest that around 40% of announced data-centre projects in the United States are affected by infrastructure-related delays—mainly due to missing grid connections.

The International Energy Agency expects global electricity consumption by data centres to reach around 1,000 TWh by the end of 2026. That is roughly equivalent to Germany’s annual electricity consumption.

The major technology companies are already responding. Microsoft has signed long-term power purchase agreements with nuclear power operators, including Three Mile Island. Where public infrastructure reaches its limits, hyperscalers are becoming energy players themselves.

For investors, this opens up an important second layer of the AI theme. It is no longer only about chips, software and cloud capacity. Increasingly, it is also about power grids, energy infrastructure, cooling, land, permits and financing.

Financing Is Changing

In the first phase of the AI boom, many investments were funded largely from operating cash flows. That picture is now changing. More and more companies are turning to debt financing.

Oracle now has more than USD 100 billion in outstanding liabilities—partly due to an USD 18 billion bond issuance to finance AI infrastructure. Specialised providers such as CoreWeave are also taking on substantial debt.

This development has two consequences. First, it increases the supply of corporate bonds and may therefore exert additional upward pressure on yields. Second, it makes the sector more sensitive to interest rates. As long as growth, utilisation and margins remain high, this is manageable. But if the interest-rate cycle deteriorates or demand disappoints, vulnerability increases.

The AI Boom Is More Global Than It Appears

Although the AI cycle is often perceived as a US phenomenon, its value chain is global. A significant share of high-quality hardware—particularly advanced semiconductors, memory and components—is produced outside the United States.

Taiwan and South Korea are among the most important beneficiaries. The American investment boom is therefore acting like a global import engine.

This supports our overweight position in emerging markets. What often appears in equity markets as a US technology theme is, in terms of real value creation, an international event. For investors, this means that opportunities are also emerging along global supply chains.

SoundCapital Positioning

We are maintaining our overall positioning. At the same time, we are sharpening our focus where recent market developments warrant it.

Bonds

Within fixed income, we remain overweight high-quality corporate bonds. Tight credit spreads confirm our cautious stance on high-yield bonds.

On duration, we are deliberately taking a countercyclical approach. We are using the recent rise in yields in EUR, USD and GBP to increase duration slightly in these currencies. This serves two objectives: first, it locks in attractive yield levels for several years; second, it creates a buffer for periods in which growth expectations may unexpectedly deteriorate.

In Swiss francs, by contrast, we remain cautious due to the low level of yields.

Equities

Our regional overweight in emerging markets remains in place. The data on the global value creation of the AI boom confirms this assessment. Valuations, positioning and structural growth continue to argue in favour of the region.

We also maintain our exposure to the structural themes of artificial intelligence, big data and energy infrastructure. These are no longer merely long-term growth expectations, but increasingly real-economy drivers with a robust fundamental basis.

Alternative Investments

Gold retains its role as a diversifier in an environment of heightened political and monetary-policy uncertainty. Market-neutral hedge funds also remain an important stabiliser and have once again demonstrated their diversification benefits during the recent market phase.

Final Thought

The AI boom is no longer merely a story about future possibilities. It has become measurable—in earnings figures, investment budgets, order backlogs, GDP statistics and yield curves.

That is precisely what makes it a serious macroeconomic force.

For investors, this creates a dual task: remain invested in the structural winners—while closely monitoring the side effects. These include higher interest rates, bottlenecks in power and grid infrastructure, and rising leverage among individual players.

The numbers are now speaking clearly. The task is to listen carefully.

Appendix & Disclaimer

SoundInsights is the central tool for our investment allocation. We use it to systematically and consistently assess the aspects that are relevant to the development of the financial markets. As a result, our clients can rely on a rational and anti-cyclical implementation of our investment decisions.

- Focusing on the essentials

Interest rate level, risk premium, valuation, economic development, investor sentiment and positioning. These are the decisive factors for success on the financial markets, especially in turbulent times when the temptation to react irrationally to the headlines is particularly strong. - Comparability over time and place

The factors mentioned above are equally relevant for all markets and at all times. This is the result of a strict «backtesting» process that continues into the future. - Cumulating our investment experience

Our strength lies in the many years of experience of our partners and principals. It is precisely this experience that we summarize and make it applicable with SoundInsights. - Transparency

Thanks to our monthly publication, our clients always know where we stand in the investment cycle and how we expect the financial markets to develop.

This document is an advertisement and is intended solely for information purposes and for the exclusive use by the recipient. This document was produced by SoundCapital (hereafter «SoundCapital») with the greatest of care and to the best of its knowledge and belief. However, SoundCapital does not warrant any guarantee with regard to its correctness and completeness and does not accept any liability for losses that might occur through the use of this information. This document does not constitute an offer or a recommendation for the purchase or sale of financial instruments or services and does not discharge the recipient from his own judgment. Particularly, it is recommended that the recipient, if needed by consulting professional guidance, assess the information in consideration of his personal situation with regard to legal, regulatory and tax consequences that might be invoked. Although information and data contained in this document originate form sources that are deemed to be reliable, no guarantee is offered regarding the accuracy or completeness. A past performance of an investment does not constitute any guarantee of its performance in the future. Performance forecasts do not serve as a reliable indicator of future results. This document is expressly not intended for persons who, due to their nationality or place of residence, are not permitted access to such information under local law. It may not be reproduced either in part or in full without the written permission of SoundCapital.

© 2026 SoundCapital. All rights reserved.

Datasource: Bloomberg