SC — INSIGHTN°48

SoundInsightN°42

01

Oil price shock likely to be temporary

02

The Strait of Hormuz as the key risk factor

03

Investment strategy remains defensively positioned

04

Precious metals exhibiting extreme volatility

Bonds

Overview

Interest Rates

Credit Spreads

UnattractiveAttractive

Equities

Overview

+1

Equity Risk Premium

Leading Indicators

Risk Index

UnattractiveAttractive

Posted 3/3/2026 by Christian Luchsinger

Geopolitical Escalation in the Middle East

Just days ago, headlines were dominated by legal setbacks for Donald Trump over trade tariffs. The U.S. Supreme Court declared key punitive tariffs unlawful—a signal of both political and economic significance. That narrative has since been overtaken by escalating tensions surrounding Iran, developments that could carry far more persistent global economic consequences.

What Happened?

Over the weekend, the United States and Israel conducted coordinated strikes against targets in Iran. The attacks followed months of negotiations over a renewed nuclear agreement, which, from Washington’s perspective, failed to produce a satisfactory outcome.

According to official statements, the air and missile strikes targeted military and nuclear infrastructure. Media reports indicate that Iran’s Supreme Leader, Ali Khamenei, was killed in the operation. Tehran responded with retaliatory attacks against Israeli and U.S. military positions in the region.

The situation remains tense—and economically relevant.

Oil Prices as the Transmission Channel

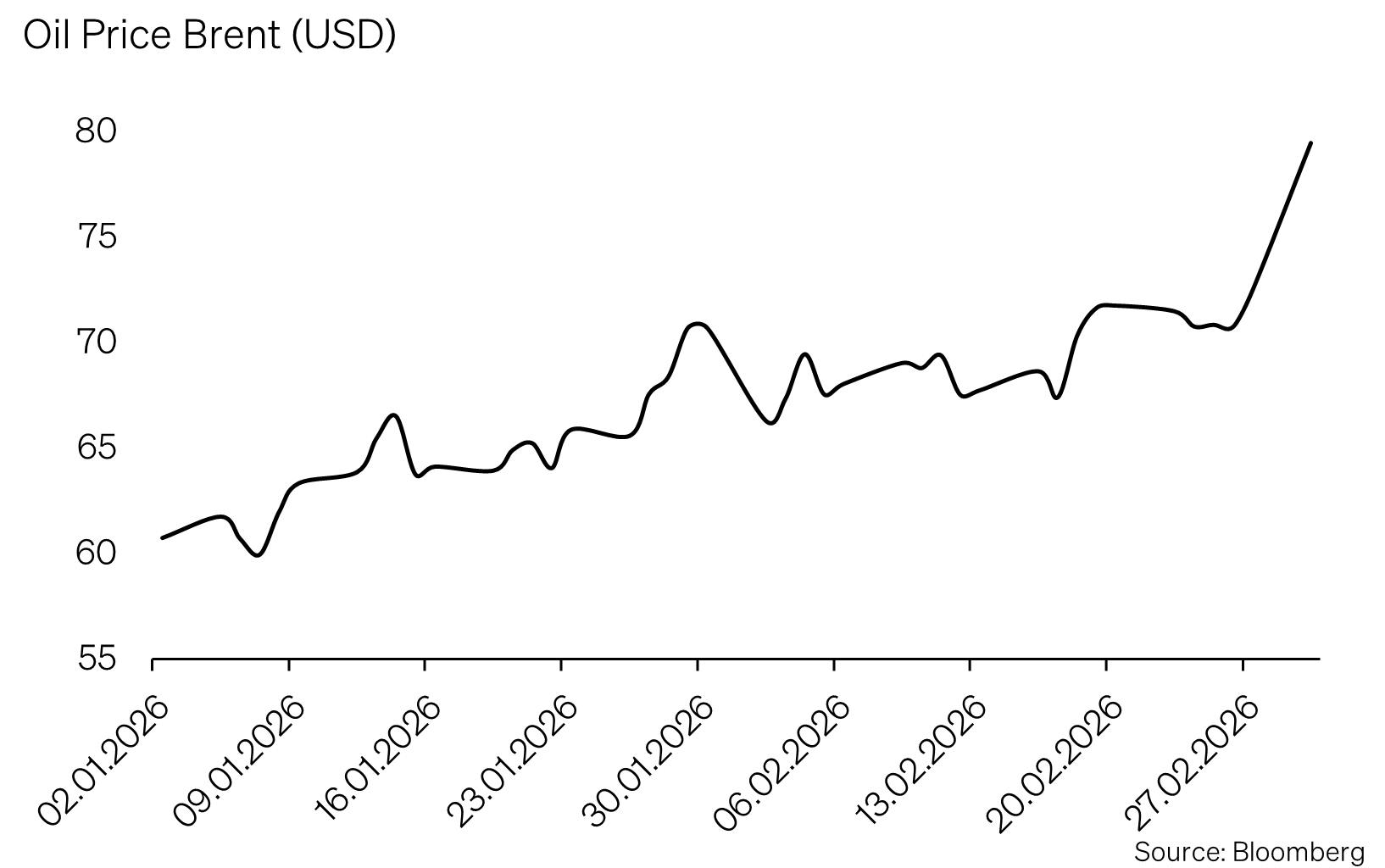

The most immediate economic impact of the conflict is visible in energy markets. Brent crude rose by roughly 9% following the escalation. Analysts estimate that a contained military confrontation could add approximately USD 10–15 per barrel on a temporary basis.

Yet the initial market reaction is less important than the question of physical supply disruption. Price spikes driven by headlines tend to fade. Sustained interruptions to production or transportation infrastructure would be a different matter entirely.

The Strategic Chokepoint: The Strait of Hormuz

At the center of the geopolitical calculus lies the Strait of Hormuz—one of the world’s most critical energy transit routes. Roughly one-fifth of global oil and LNG trade passes through this narrow waterway.

Even partial disruptions could trigger additional risk premiums in energy markets. A prolonged blockade, however, would have tangible global economic consequences. That said, the oil market is not currently characterized by structural undersupply. As long as shipping lanes remain open, price spikes may prove contained.

Macroeconomic Implications

For inflation and growth, the duration of an oil shock matters more than its magnitude. A 10% increase in oil prices would likely lift U.S. headline inflation by only a few tenths of a percentage point on a temporary basis, while core inflation would remain largely unaffected.

Central banks typically respond to sustained shifts in inflation expectations—not to one-off energy impulses. Unless higher oil prices become entrenched and spill over into wages and broader pricing dynamics, the macroeconomic fallout should remain manageable.

Elevated Valuations Meet Rising Uncertainty

U.S. equities are currently trading above the historical valuation averages seen during previous oil crises. This increases vulnerability to sudden bouts of risk aversion.

However, the still-moderate level of market volatility suggests that investors are, for now, pricing in a limited escalation rather than a prolonged regional conflict.

Political-Economic Realities

Sustainably high oil prices would carry political and inflationary costs—not only for the United States. Accordingly, multiple stakeholders share a strong incentive to prevent an uncontrolled escalation spiral.

Given that the military initiative originated in Washington, pressure is likely mounting there as well to stabilize the region swiftly.

The immediate economic dimension reinforces this urgency. Dubai—currently the world’s largest international aviation hub—is effectively grounded. Air traffic through one of the most important transit nodes between Europe, Asia, and Africa has been severely restricted.

Dubai is not merely a tourism center; it is a critical junction for global supply chains, business travel, and air freight. The disruption of such core infrastructure underscores the economic imperative for rapid de-escalation—regionally and globally.

Investor Perspective

Historically, commodity-driven shocks stemming from regionally contained conflicts have triggered short-term market reactions but rarely resulted in lasting structural breaks—provided no sustained supply disruptions occurred.

The decisive factor is the physical dimension of the conflict, not the media narrative. For investors, elevated volatility reflects uncertainty—not necessarily structural repricing.

In comparable situations, phases of pronounced risk aversion have often proven more opportunistic than transformational. The current environment warrants close monitoring—but not premature strategic repositioning.

Investment Committee Positioning

No tactical adjustments were made in February. Despite heightened geopolitical tensions, we currently see no reason for a fundamental portfolio realignment.

Fixed Income

Our focus remains on high-quality corporate bonds. Investment-grade issuers with robust balance sheets and reliable cash flows are preferred. We deliberately avoid high-yield bonds and subordinated structures. Given tight credit spreads, the incremental yield offered by lower-quality segments does not appear adequately compensated.

In private credit markets, several recent cases have raised transparency concerns. Reports of alleged “double pledging”—the practice of using identical collateral for multiple loans—highlight structural vulnerabilities. The rapid growth of private debt markets has occurred partly outside traditional banking regulatory frameworks. Periods of market stress tend to expose such weaknesses more clearly. An escalation of the situation could create opportunities; however, we currently have no direct exposure.

Equities

Equity positioning remains unchanged. We continue to emphasize energy infrastructure, quality dividend stocks, and selected companies in the artificial intelligence ecosystem. These segments combine structural growth drivers with solid underlying fundamentals.

The protective put options initiated in January proved effective amid heightened volatility. Given the recent rise in implied volatility, we tactically realized the position and will discuss further measures going forward.

Alternatives

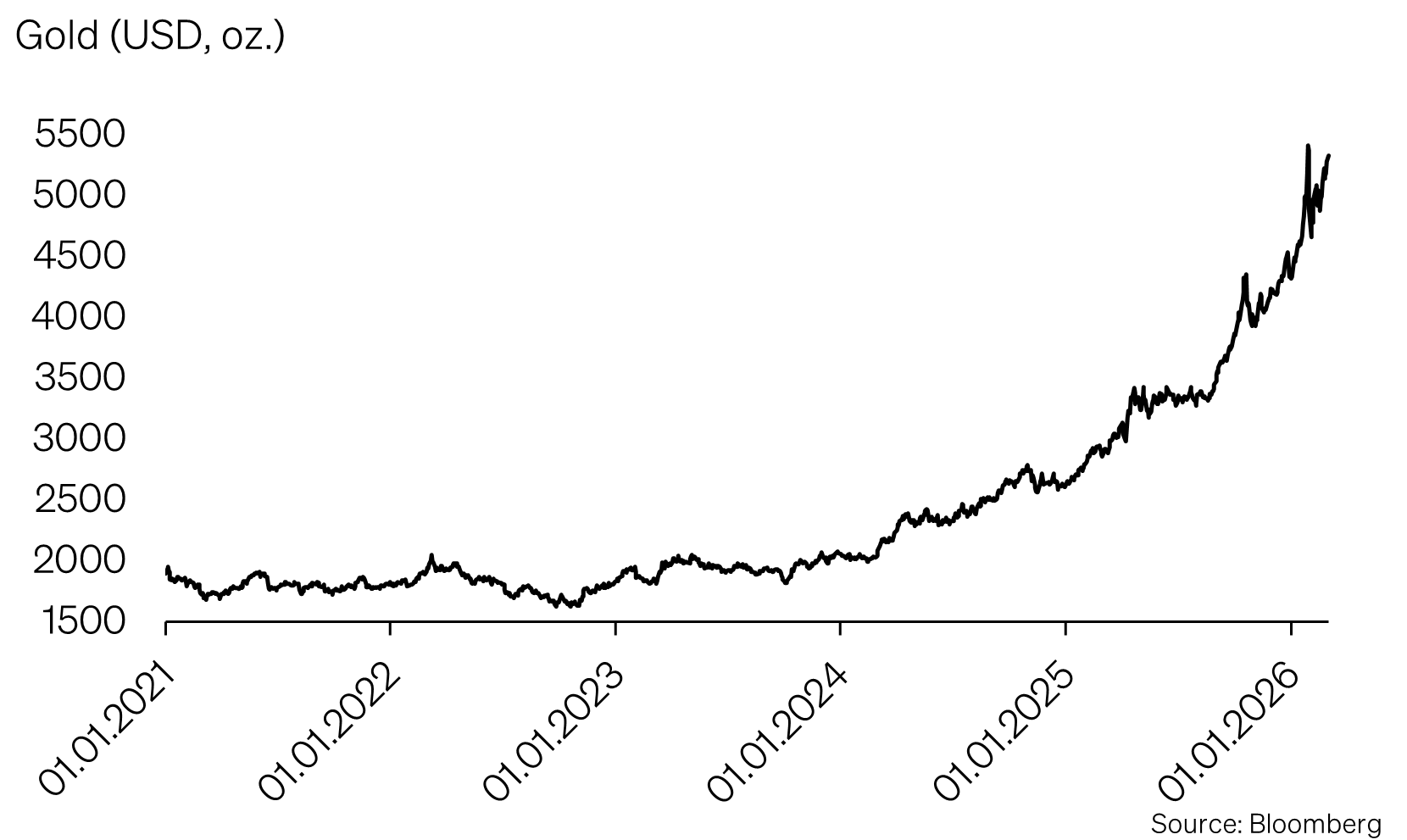

Gold rallied strongly at the beginning of the year—at times up nearly 30%—before correcting by roughly 22%. Silver exhibited even more pronounced volatility, temporarily losing almost 50% within a few trading days—an historically exceptional move in terms of speed.

Such swings often reflect technical factors: elevated speculative positioning, leverage structures, and one-sided market sentiment. When psychology shifts abruptly, price movements can amplify themselves.

Over the long term, precious metals continue to serve a diversification function—particularly during periods of elevated geopolitical uncertainty. In the short term, however, overshooting can typically occur, as these markets are driven more by capital flows than by recurring income streams.

From a strategic perspective, the key distinction remains between structural hedging benefits and tactical market mechanics.

Appendix & Disclaimer

Mit SoundInsights beurteilen wir systematisch und konsistent die Aspekte, die für die Entwicklung der Finanzmärkte relevant sind. In der Folge können sich unsere Kunden auf eine rationale und antizyklische Umsetzung unserer Anlageentscheidungen verlassen.

- Konzentration auf das Wesentliche

Zinsniveau, Risikoaufschlag, Bewertung, Wirtschaftsentwicklung, Anlegerstimmung und -positionierung. Das sind die zentralen Faktoren. Sie entscheiden über den Erfolg an den Finanzmärkten. Besonders in turbulenten Zeiten, wenn die Versuchung besonders gross ist, irrational den Schlagzeilen hinterherzulaufen. - Vergleichbarkeit über Ort und Zeit

Die genannten Faktoren sind für alle Märkte und zu jeder Zeit gleichermassen relevant. Dies ergab sich aus einem strengen «Backtesting», welches sich rollend in die Zukunft fortsetzt. - Bündeln unserer kumulierten Anlageerfahrung

Unsere Stärke liegt in den langjährigen Erfahrungen unserer Partner und Principals. Genau diese Erfahrungen fassen wir zusammen und machen sie mittels SoundInsights anwendbar. - Transparenz

Durch die monatliche Publikation wissen unsere Kunden stets, wo wir im Anlagezyklus stehen und wohin die Reise an den Finanzmärkten geht.

Das vorliegende Dokument dient ausschliesslich zu Informationszwecken und ist als Werbung zu verstehen. Es wurde von SoundCapital (nachfolgend «SC») mit grösster Sorgfalt erstellt. Trotz sorgfältiger Bearbeitung übernimmt SC keine Gewähr für die Richtigkeit, Vollständigkeit oder Aktualität der enthaltenen Informationen und lehnt jegliche Haftung für Verluste ab, die durch die Nutzung dieses Dokuments entstehen könnten. Die in diesem Dokument geäusserten Meinungen spiegeln die Einschätzungen von SC zum Zeitpunkt der Erstellung wider und können sich ohne vorherige Ankündigung ändern. Es handelt sich weder um ein Angebot noch eine Empfehlung zum Kauf oder Verkauf von Finanzinstrumenten oder zur Inanspruchnahme von Dienstleistungen. Empfängern wird empfohlen, eigene Beurteilungen vorzunehmen und gegebenenfalls unter Hinzuziehung eines Beraters die Informationen in Bezug auf ihre individuellen Umstände sowie deren rechtliche, regulatorische und steuerliche Auswirkungen zu überprüfen. Obwohl die Informationen aus als zuverlässig angesehenen Quellen stammen, übernimmt SC keine Garantie für deren Genauigkeit. Vergangene Wertentwicklungen von Anlagen sind kein verlässlicher Indikator für zukünftige Ergebnisse. Ebenso sind Prognosen zur Wertentwicklung nicht als verlässlicher Indikator für künftige Ergebnisse zu verstehen. Dieses Dokument richtet sich nicht an Personen, deren Nationalität oder Wohnsitz den Zugang zu solchen Informationen rechtlich einschränkt. Eine Vervielfältigung, auch auszugsweise, ist nur mit ausdrücklicher schriftlicher Genehmigung von SC gestattet.

© 2026 SoundCapital.

Datenquelle: Bloomberg, BofA ML Research