SC — INSIGHTN°48

SoundInsightN°44

01

Markets follow fundamentals, not headlines.

02

Growth remains resilient.

03

Bottlenecks shift to energy and infrastructure.

Bonds

Overview

Interest Rates

Credit Spreads

UnattractiveAttractive

Equities

Overview

Equity Risk Premium

Leading Indicators

Risk Index

UnattractiveAttractive

Posted 4/21/2026 by Christian Luchsinger

Between Signal and Noise

Recent weeks have been dominated by geopolitical tensions surrounding Iran. News flow has been intense, uncertainty elevated, and volatility temporarily reached levels last seen following the U.S. tariff announcements on “Liberation Day”.

What stands out, however, is the market’s response: following the March correction, many risk assets rebounded quickly. Global equity markets posted several consecutive days of gains, in some cases already returning to record levels.

This raises a key question:

Are markets underestimating the risks—or are they successfully distinguishing between short-term noise and fundamental signals?

Our view: Markets are increasingly looking through near-term uncertainty (noise) and focusing on structural drivers (signal).

Noise: Transient by Nature

Geopolitical events tend to have an immediate impact. They elevate risk premia, increase volatility, and shape short-term investor behavior. The current conflict is a textbook example—particularly via the energy sector.

However, what ultimately matters is not the intensity of the reaction, but its duration. The key question is whether such events structurally impair economic momentum—or whether they remain temporary and can therefore be classified as noise.

In recent days, diplomatic efforts surrounding the Iran conflict have gained visible momentum, even though the temporary reopening of the Strait of Hormuz was subsequently reversed. Further negotiation rounds are expected, supported by international mediation initiatives.

Given the significant economic and political costs, incentives for de-escalation are rising across all sides. This reinforces a familiar pattern: even during periods of heightened tension, markets tend to anticipate the likelihood of a negotiated outcome at an early stage.

Signal: Fundamentals Remain Intact

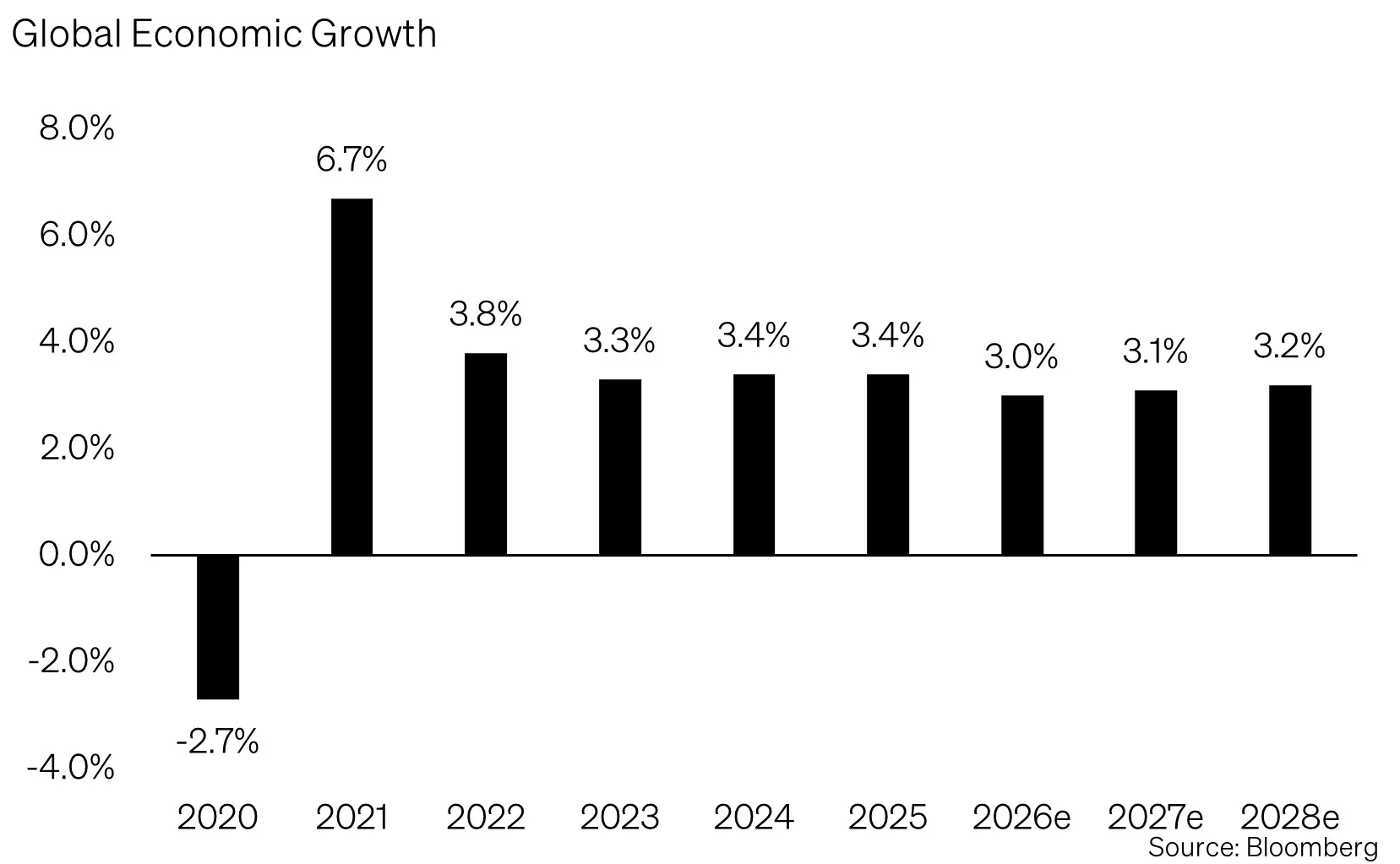

Despite geopolitical tensions, the macroeconomic backdrop remains robust. The International Monetary Fund (IMF) forecasts global growth of approximately 3.1% for 2026. While below historical peaks, this still signals a stable growth trajectory—even in a more challenging environment.

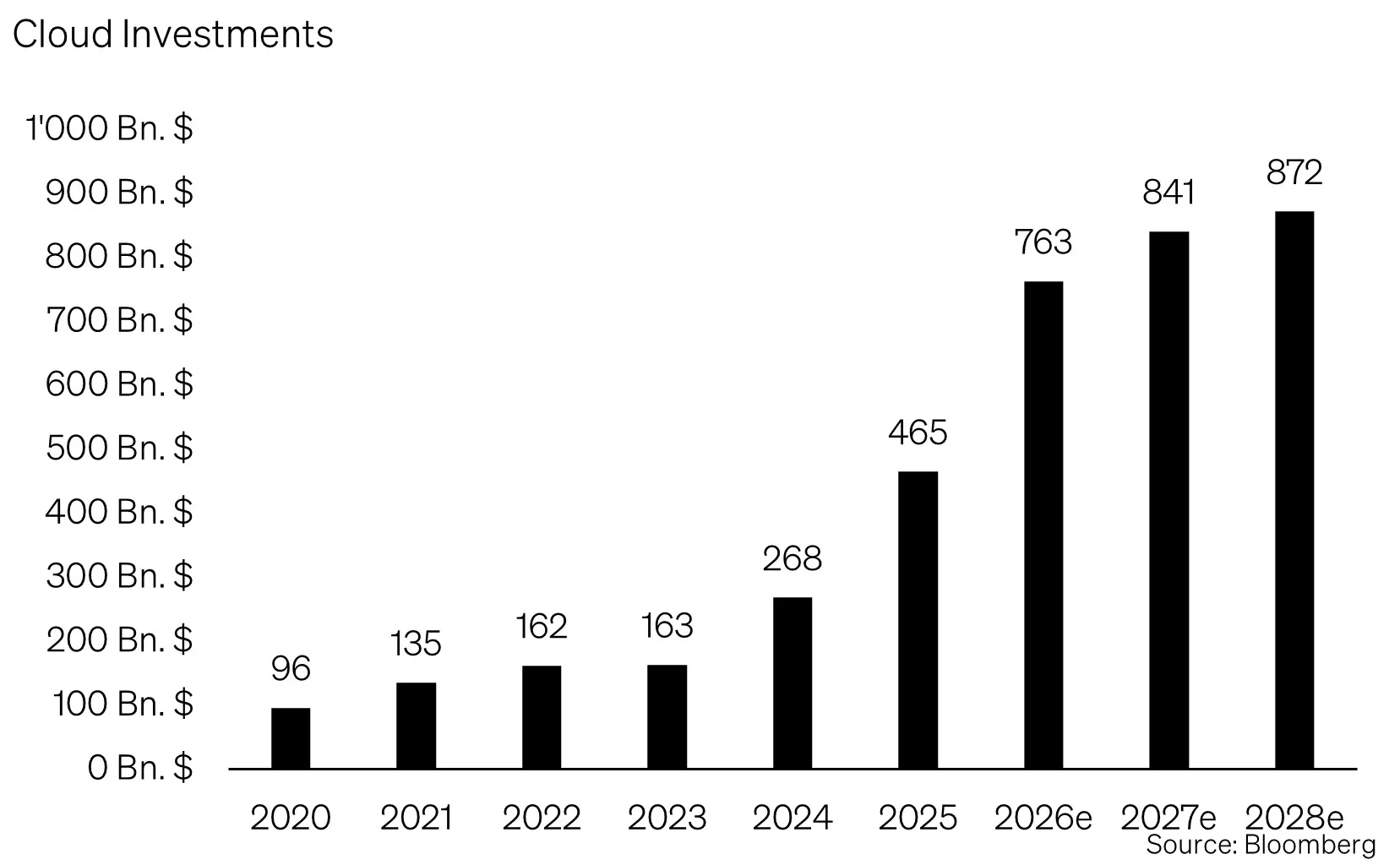

A Structurally Driven Investment Cycle

A key driver is the exceptionally strong investment cycle in digital infrastructure—an area we have long emphasized in portfolios. Major technology companies are planning capital expenditures in the hundreds of billions for 2026:

- Alphabet: USD 175–185 billion

- Meta: USD 115–135 billion

- Amazon: ~USD 200 billion

This scale highlights that we are not dealing with a short-term trend, but with a multi-year structural buildout of data centers, networks, and semiconductor capacity. What is being created here forms the backbone of the next phase of technological development.

When Digital Demand Becomes Physical

As digital infrastructure expands, so does the demand for energy and computing power. The International Energy Agency (IEA) expects sustained growth in electricity demand—driven by electrification, cooling needs, and data-intensive applications.

The key observation: the AI boom is no longer just reflected in expectations—it is materializing in real-economy investments.

Capacity Constraints as the New Bottleneck

The pace of development becomes even clearer when looking at the details. While semiconductors were initially the focus, a broader range of bottlenecks is now emerging: network infrastructure, cooling systems, and particularly energy supply.

Modern data centers now require power levels comparable to small cities. In many regions, long grid connection timelines and infrastructure limitations are causing delays of several years.

This reveals a critical shift:

The constraint is no longer capital or technology—but physical implementation.

Even with substantial planned investments, these bottlenecks are likely to persist for years—outlasting most geopolitical conflicts. For investors, this creates an attractive setup: structurally strong demand meets constrained supply, supporting sustained pricing power across the value chain.

Markets Are Weighing, Not Ignoring Risks

Market movements in recent weeks should be viewed in this context. Geopolitical risks are not being ignored—they are being assessed relative to underlying growth drivers.

Unless escalation leads to persistently higher energy prices or disrupts core economic processes, the risk of a fundamental downturn remains limited.

Importantly, the economic starting point prior to the conflict was very strong. Leading indicators pointed to expansion, and corporate earnings expectations have been revised upward consistently over recent quarters. In such an environment, exogenous shocks tend to be absorbed more effectively.

Strategy Over Reaction

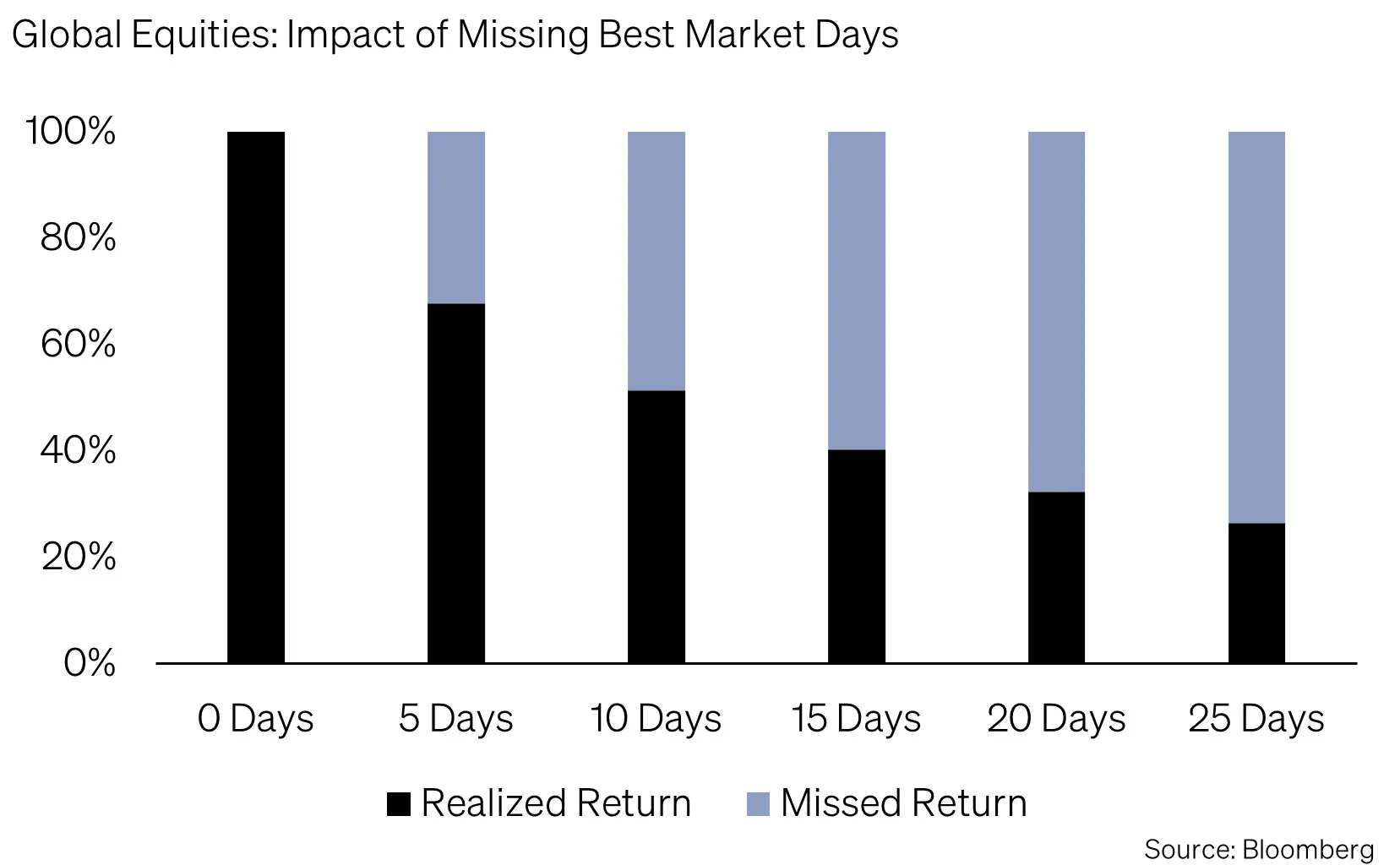

Recent days have highlighted a frequently underestimated dynamic: the strongest market days often occur close to the weakest.

Reducing exposure during volatile periods risks missing these recovery phases—often with meaningful consequences for long-term returns.

This pattern has been evident repeatedly and underscores the importance of discipline when navigating short-term market fluctuations.

SoundCapital Positioning: Deliberately Unchanged

The March market movements represented an initial stress test for 2026. Our positioning proved resilient during this phase. As a result, the investment committee has consciously decided to maintain the current allocation.

Fixed Income

We remain overweight high-quality corporate bonds. Current tight credit spreads support our cautious stance toward riskier segments, particularly high yield.

Overall duration is kept neutral. We are monitoring interest rate developments selectively: rising USD yields may present opportunities, while in CHF we remain cautious due to low yield levels. In EUR, the rate environment has improved, offering increasingly attractive long-term return potential.

Equities

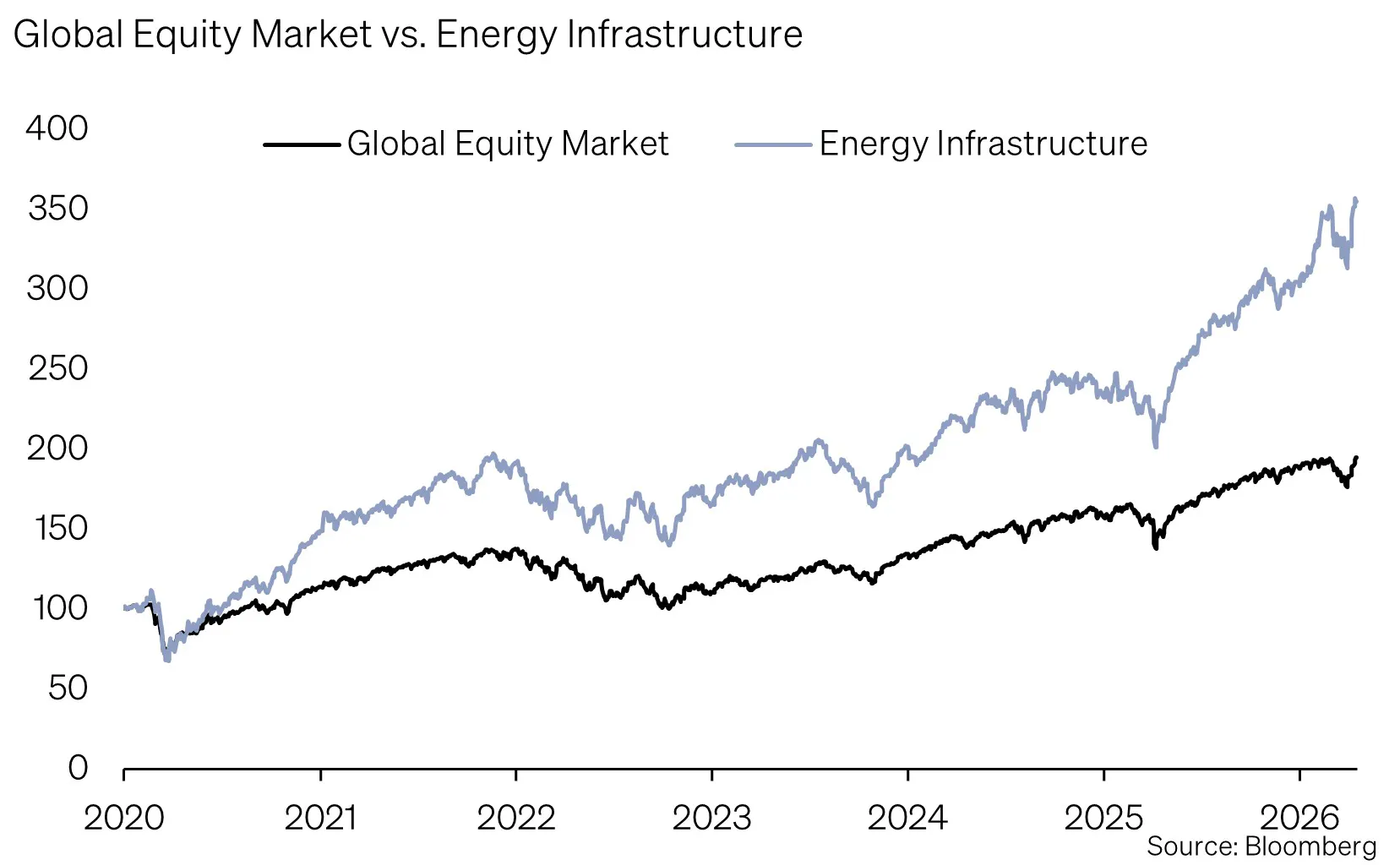

Within equities, our regional focus remains on emerging markets. In our view, attractive valuations, still-cautious investor positioning, and superior long-term growth potential continue to support the region.

Additionally, we maintain exposure to structural themes such as artificial intelligence, big data, and energy infrastructure.

Alternatives

Alternative investments continue to provide stability. Gold remains an effective geopolitical hedge, while market-neutral hedge funds have once again demonstrated their diversification benefits during periods of volatility.

We therefore remain positioned to capture opportunities. Volatility is not viewed primarily as a risk, but as a potential opportunity to selectively increase exposure.

Closing Thought

The key challenge for investors today is not to avoid uncertainty—but to interpret it correctly.

In an environment defined by rapid news cycles, the ability to differentiate becomes critical:

What is short-term noise—and what constitutes a long-term signal?

Current market behavior suggests that this distinction is being made with notable precision.

Appendix & Disclaimer

Mit SoundInsights beurteilen wir systematisch und konsistent die Aspekte, die für die Entwicklung der Finanzmärkte relevant sind. In der Folge können sich unsere Kunden auf eine rationale und antizyklische Umsetzung unserer Anlageentscheidungen verlassen.

- Konzentration auf das Wesentliche

Zinsniveau, Risikoaufschlag, Bewertung, Wirtschaftsentwicklung, Anlegerstimmung und -positionierung. Das sind die zentralen Faktoren. Sie entscheiden über den Erfolg an den Finanzmärkten. Besonders in turbulenten Zeiten, wenn die Versuchung besonders gross ist, irrational den Schlagzeilen hinterherzulaufen. - Vergleichbarkeit über Ort und Zeit

Die genannten Faktoren sind für alle Märkte und zu jeder Zeit gleichermassen relevant. Dies ergab sich aus einem strengen «Backtesting», welches sich rollend in die Zukunft fortsetzt. - Bündeln unserer kumulierten Anlageerfahrung

Unsere Stärke liegt in den langjährigen Erfahrungen unserer Partner und Principals. Genau diese Erfahrungen fassen wir zusammen und machen sie mittels SoundInsights anwendbar. - Transparenz

Durch die monatliche Publikation wissen unsere Kunden stets, wo wir im Anlagezyklus stehen und wohin die Reise an den Finanzmärkten geht.

Das vorliegende Dokument dient ausschliesslich zu Informationszwecken und ist als Werbung zu verstehen. Es wurde von SoundCapital (nachfolgend «SC») mit grösster Sorgfalt erstellt. Trotz sorgfältiger Bearbeitung übernimmt SC keine Gewähr für die Richtigkeit, Vollständigkeit oder Aktualität der enthaltenen Informationen und lehnt jegliche Haftung für Verluste ab, die durch die Nutzung dieses Dokuments entstehen könnten. Die in diesem Dokument geäusserten Meinungen spiegeln die Einschätzungen von SC zum Zeitpunkt der Erstellung wider und können sich ohne vorherige Ankündigung ändern. Es handelt sich weder um ein Angebot noch eine Empfehlung zum Kauf oder Verkauf von Finanzinstrumenten oder zur Inanspruchnahme von Dienstleistungen. Empfängern wird empfohlen, eigene Beurteilungen vorzunehmen und gegebenenfalls unter Hinzuziehung eines Beraters die Informationen in Bezug auf ihre individuellen Umstände sowie deren rechtliche, regulatorische und steuerliche Auswirkungen zu überprüfen. Obwohl die Informationen aus als zuverlässig angesehenen Quellen stammen, übernimmt SC keine Garantie für deren Genauigkeit. Vergangene Wertentwicklungen von Anlagen sind kein verlässlicher Indikator für zukünftige Ergebnisse. Ebenso sind Prognosen zur Wertentwicklung nicht als verlässlicher Indikator für künftige Ergebnisse zu verstehen. Dieses Dokument richtet sich nicht an Personen, deren Nationalität oder Wohnsitz den Zugang zu solchen Informationen rechtlich einschränkt. Eine Vervielfältigung, auch auszugsweise, ist nur mit ausdrücklicher schriftlicher Genehmigung von SC gestattet.

© 2026 SoundCapital.

Datenquelle: Bloomberg, BofA ML Research