SoundInsightN°43

Bonds

Equities

Petroflation

The conflict with Iran has entered its fourth week, with no sign of a rapid de-escalation. The longer tensions persist, the more attention shifts to their economic consequences—and with that, to rising uncertainty across capital markets.

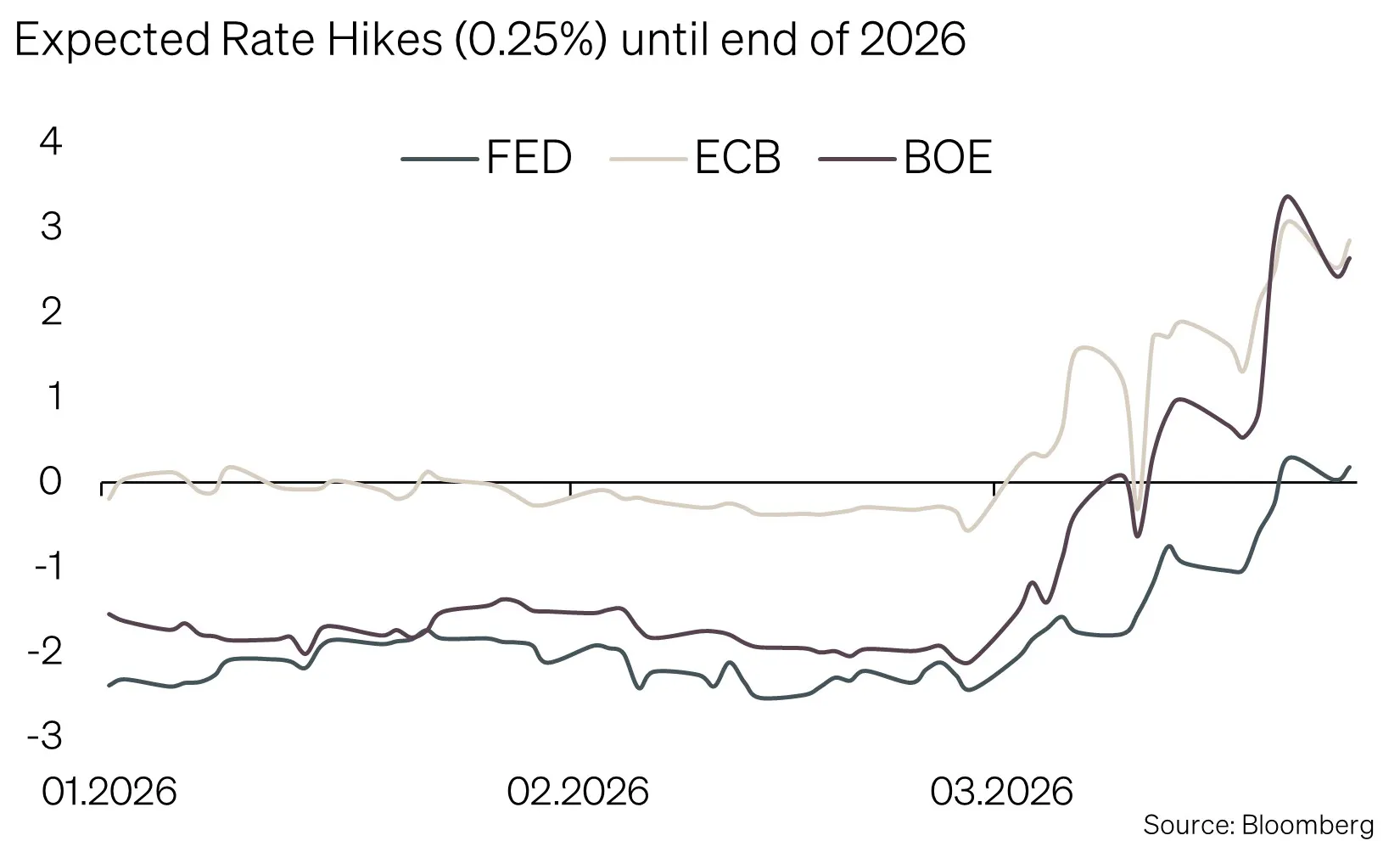

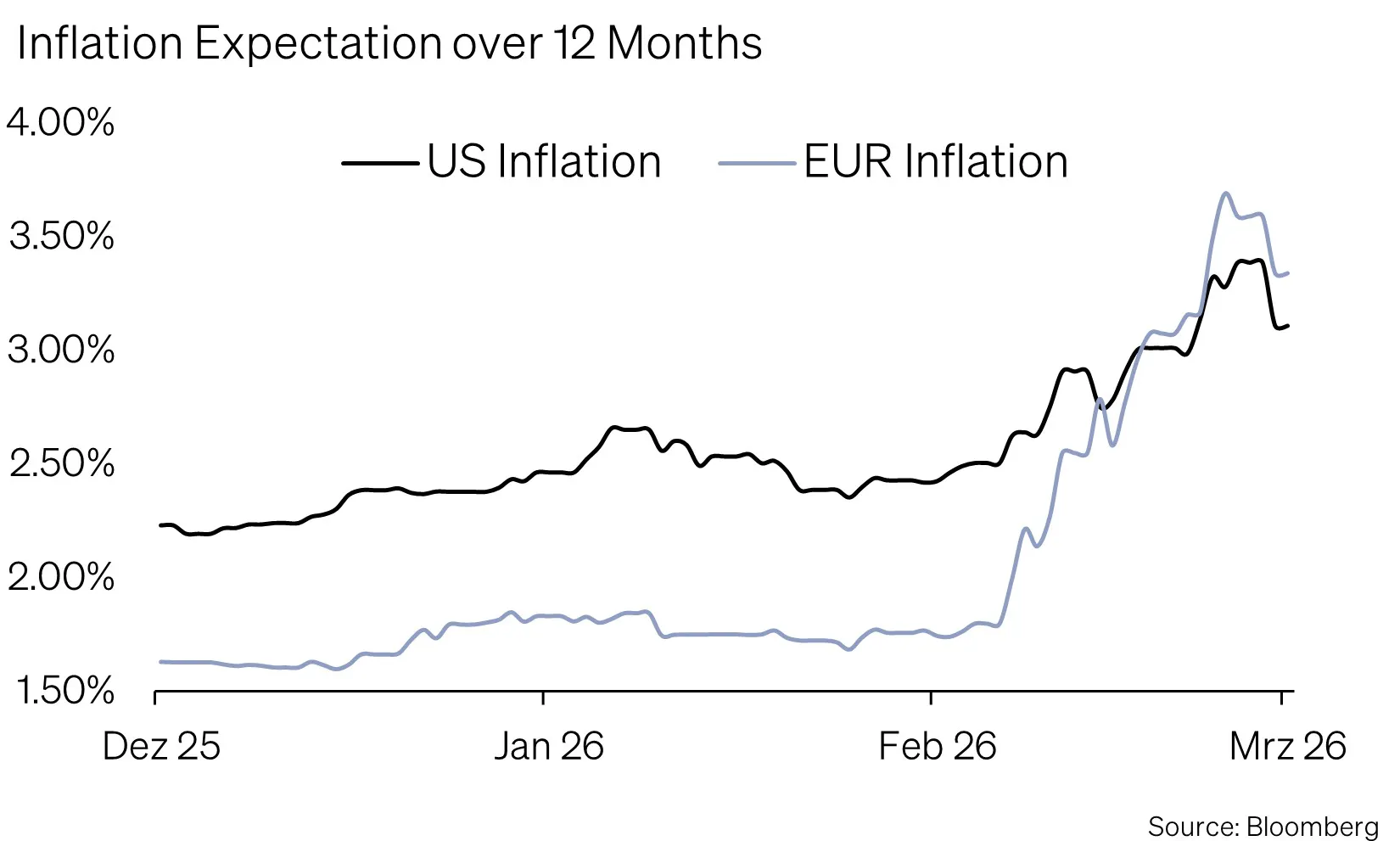

At the centre of the current debate is the return of inflation risk. Geopolitical tensions are exerting upward pressure on prices, particularly through energy markets and supply-chain disruptions. As a result, interest-rate expectations in both Europe and the United States have moved materially higher. While rate cuts were still the dominant theme at the start of the year, markets are now increasingly pricing in a scenario of higher rates for longer—with clear upside risks in Europe.

This reassessment comes at a time of growing concern about the economic outlook. Higher prices, combined with tighter financing conditions, are weighing on consumption and dampening growth prospects.

At the same time, history argues against drawing overly hasty conclusions. Geopolitical conflicts typically trigger short-term volatility, but only rarely lead to lasting structural market dislocations. For investors, the focus therefore shifts to the disciplined use of opportunities during periods of elevated uncertainty.

Energy Supply and Market Implications

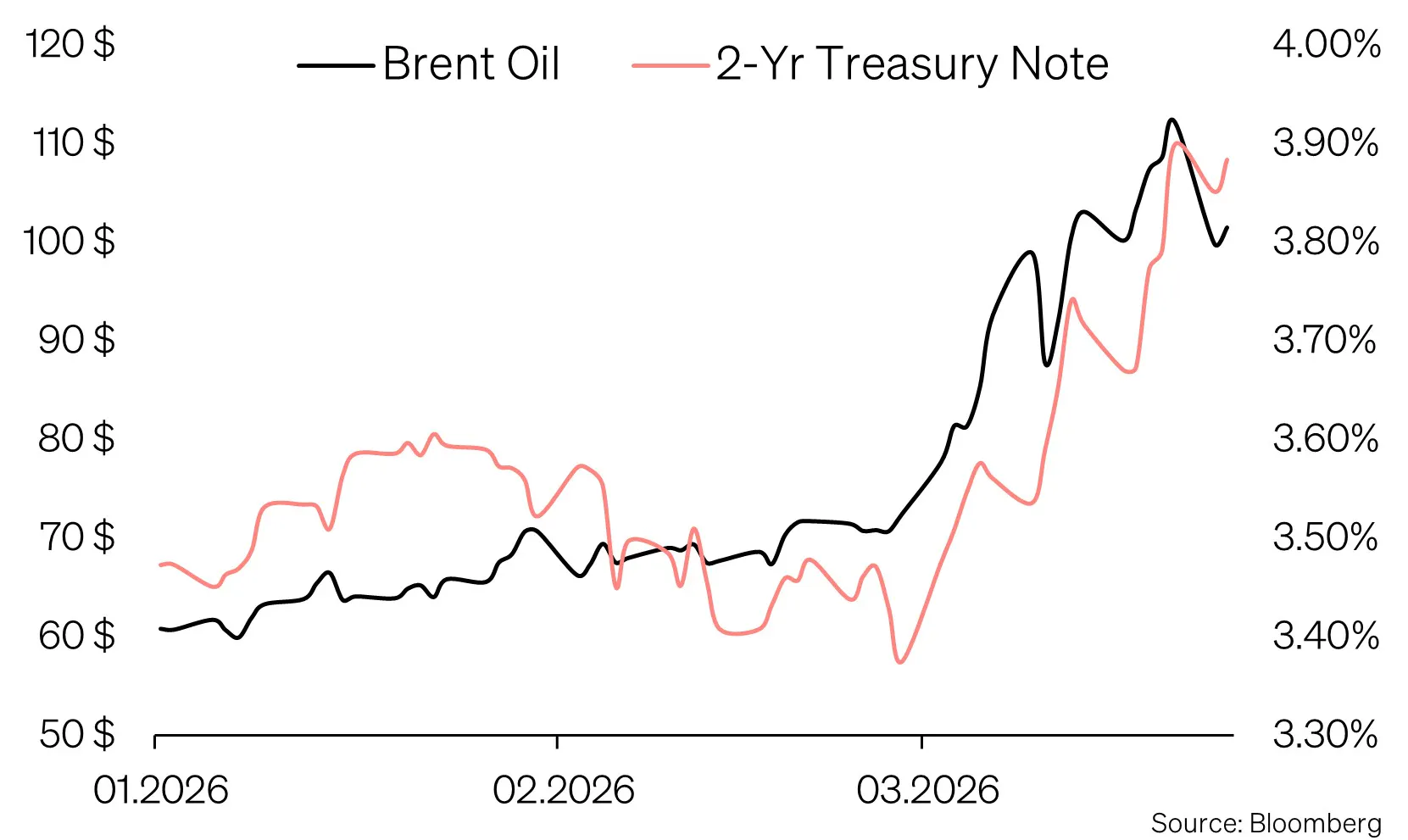

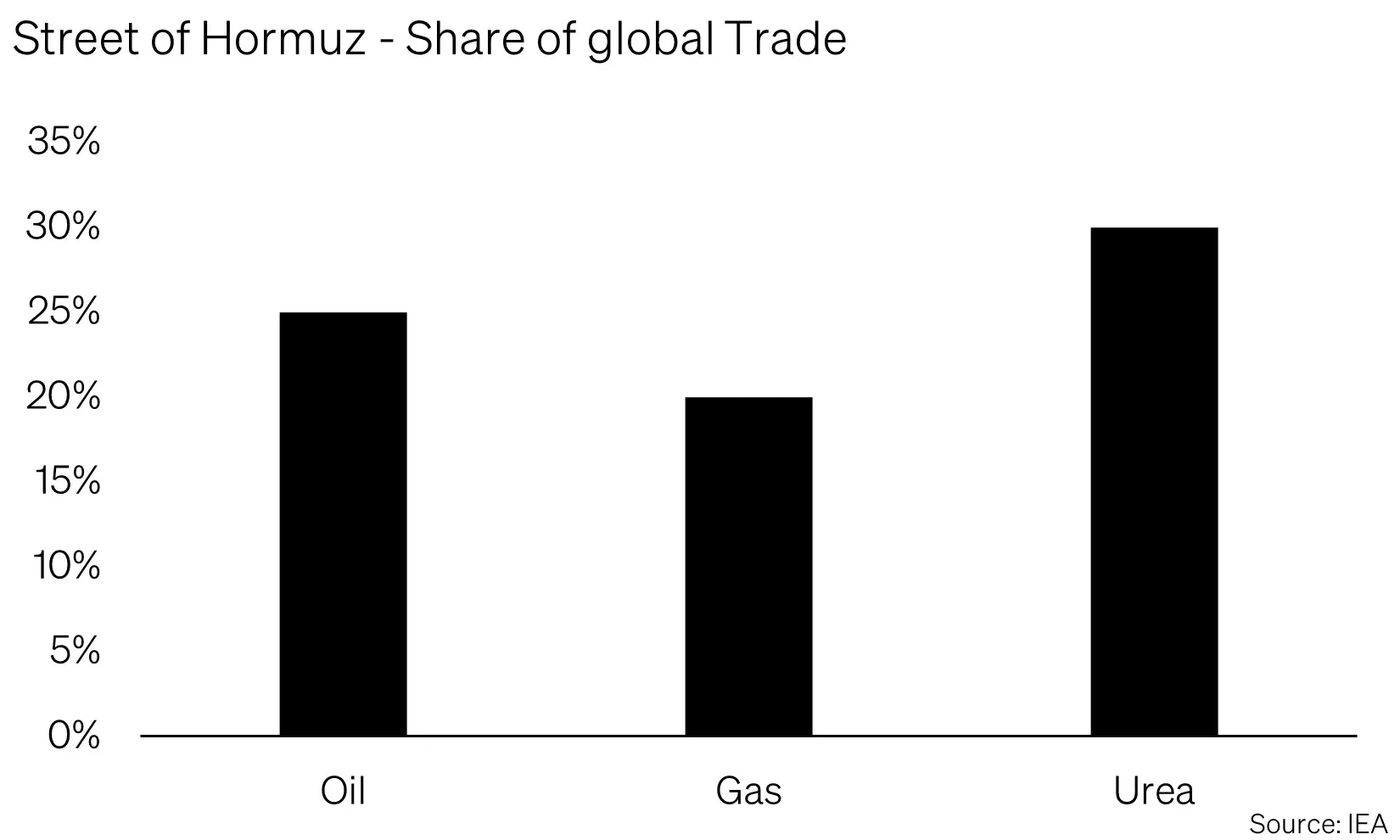

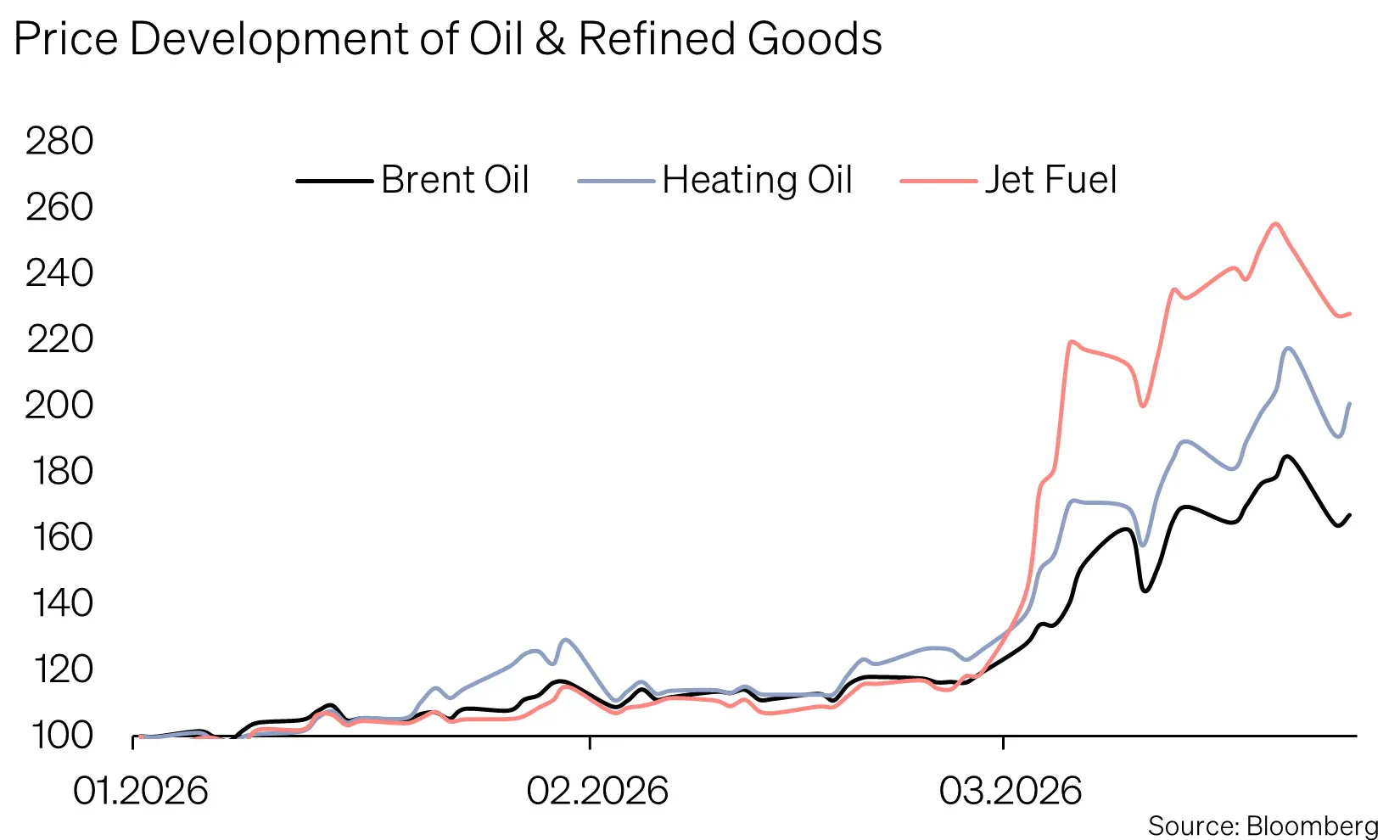

According to assessments by the International Energy Agency, the blockade of the Strait of Hormuz represents one of the most severe oil supply disruptions in modern history. Roughly 25% of global seaborne oil trade passes through this route. At the same time, the disruption affects significant parts of global gas and fertiliser trade.

The implications extend far beyond the energy sector. Crude oil and gas supply is constrained in the near term, while price moves in refined products such as diesel and jet fuel have already become significantly more pronounced. The regional impact is particularly acute in Asia, which absorbs the majority of energy flows from the Gulf.

Through higher energy prices, rising production costs and pressure on food supply chains, however, the second-round effects remain global. Strategic reserves may provide short-term stabilisation. Even so, a supply deficit is beginning to emerge, and its macroeconomic costs are likely to increase the longer the conflict persists.

Capital markets have already begun to respond. Yields on 10-year US Treasuries have risen from below 4% in February to temporarily above 4.4%. At the same time, monetary policy expectations have shifted materially: in the US, rate cuts this year are now seen as increasingly unlikely, while in the euro area markets are pricing in two to three rate hikes.

This creates a more challenging backdrop for equities. Higher rates and higher inflation simultaneously weaken both growth prospects and valuation support.

Assessment and Analysis

The current escalation is exceptional both in its geopolitical significance and in its potential macroeconomic consequences. At its core lies the risk that an external energy shock could bring inflation—a theme that had already started to recede—back to the forefront.

The transmission mechanism is clear. Higher oil and gas prices initially raise the direct cost of fuel, electricity and heating. In a second step, production, transportation and logistics costs rise. This puts pressure on real incomes and weakens demand, particularly in consumer-driven economies.

Slowing consumption, in turn, weighs on growth while increasing pressure on corporate margins. It is precisely this combination that makes the current environment so challenging: rising inflation alongside weakening growth raises the risk of a stagflationary backdrop.

Energy-intensive industries are particularly exposed, but so are globally interconnected supply chains. Constraints in LNG supply can impair electricity generation and affect industrial processes all the way through to semiconductor production. Risks of supply shortages are also rising in metals and agricultural markets.

Against this backdrop, the current market weakness is understandable. At this stage, it primarily reflects a repricing of inflation, interest rates and growth—not yet a clear recession signal.

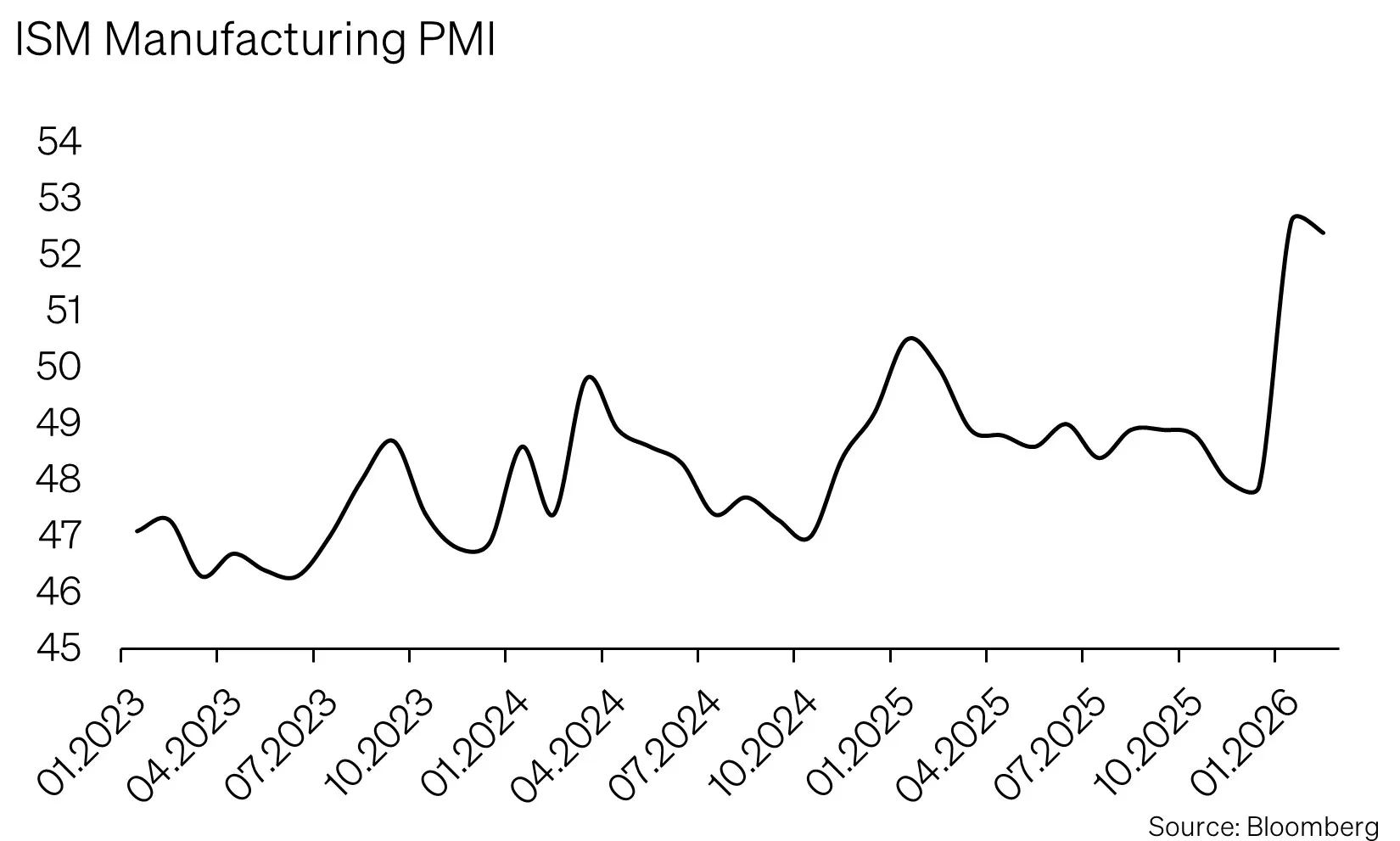

The starting point is especially important. At the beginning of the month, the macroeconomic backdrop still looked constructive: purchasing managers’ indices pointed to a recovery in economic activity, while corporate reporting continued to confirm solid earnings momentum. In other words, the conflict is hitting the global economy not in recession, but during a phase of relative stabilisation.

With each additional day of disruption in oil trade, however, the risk of non-linear knock-on effects rises. The critical issue is not crude oil prices alone, but the availability of refined products. Diesel, jet fuel and fuel oil are essential for transport and logistics and have already reacted far more sharply than crude itself. At the same time, refineries need time to adjust capacity. The longer the conflict persists, the more fragile this balance becomes.

Early signs of real-economy stress are already visible. In Pakistan, around 60% of the state vehicle fleet has reportedly been taken out of service in an effort to ration fuel. This illustrates how quickly an energy shock can translate into political and economic pressure.

Geopolitically, the situation also remains fragile. While signs of possible de-escalation are increasing, the overall stance—particularly from the United States—remains contradictory. Iran currently maintains that the Strait of Hormuz remains selectively passable; some shipments, especially to Asia, have continued. This underlines that energy flows are being used as a geopolitical lever.

SoundCapital’s Positioning

Our investment committee is closely monitoring current developments and continuously assessing their implications for portfolios. Even before the latest escalation, positioning had already been deliberately tilted defensively, reflecting elevated macroeconomic uncertainty and demanding valuations in certain parts of the market.

This starting position allows us to view the current phase of heightened volatility not only as a risk, but also as a source of opportunity. Equity exposure remains neutral, portfolios are broadly diversified, and flexibility is being deliberately preserved in order to respond to market dislocations as they arise.

Within equities, the focus remains on high-quality companies with resilient business models, stable cash flows and reliable dividend profiles. In addition, we continue to favour structural growth themes, particularly in areas such as energy infrastructure and artificial intelligence.

In fixed income, a sharp rise in yields combined with wider credit spreads—particularly in the US—can once again create attractive return opportunities. Within credit, positioning remains selective. High-yield bonds are currently being avoided, as spreads remain historically tight despite recent events.

Our investment approach remains unchanged: periods of heightened volatility are used to build positions gradually and with discipline. At the same time, we consciously avoid excessive tactical activism during phases of market stress. The priority is to add risk opportunistically where market moves overshoot fundamentals.

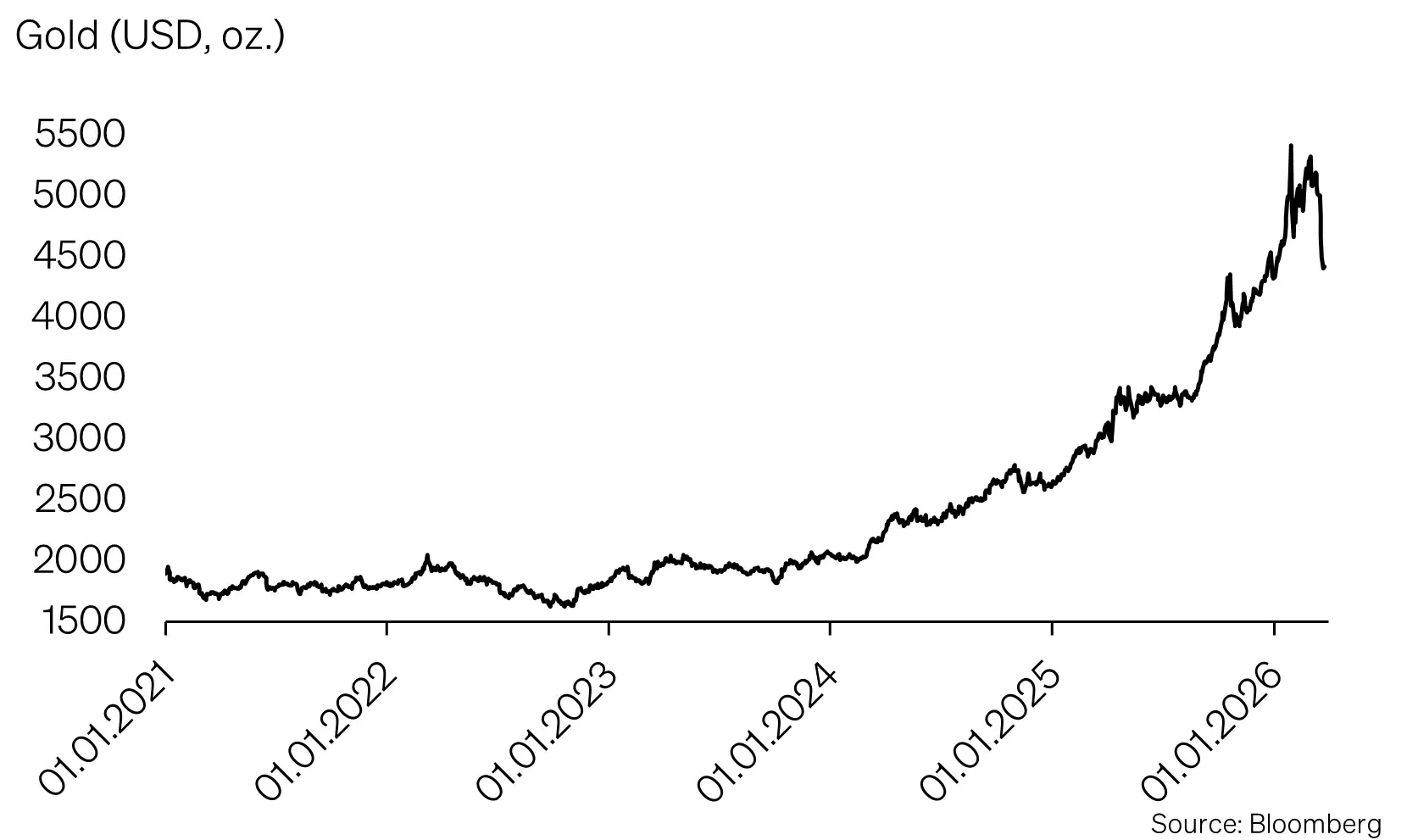

Gold: Short-Term Pressure, Long-Term Support

Alternative assets continue to play an important role, particularly because of their lower correlation with traditional asset classes.

Rising nominal and real yields are currently increasing the opportunity cost of holding gold, which has triggered pronounced profit-taking. Temporary setbacks are not unusual in an environment of higher yields.

Even so, gold remains fundamentally well supported in a backdrop of geopolitical escalation and persistent inflation concerns. As a safe-haven asset, the metal tends to benefit when uncertainty rises and confidence in macroeconomic stability deteriorates.

As long as geopolitical risks remain elevated and inflation concerns do not fully recede, gold is likely to retain its role as a diversifier, a store of real value and a stabilising anchor within portfolios.

The Bigger Picture: Equities Remain Central

However dominant geopolitical tensions and inflation risks may be in shaping short-term market behaviour, the long-term perspective remains decisive for investors. Short-term shocks can change sentiment, but they do not alter the underlying logic of long-term wealth creation.

From a strategic perspective, equities remain the most effective long-term hedge against inflation. Companies with pricing power, resilient business models and structural growth potential are generally able to pass on rising costs over time and increase nominal earnings.

For investors, the implication is clear: political and macroeconomic risks need to be assessed carefully, but they should not dominate long-term asset allocation decisions. Especially in periods of heightened uncertainty, broadly diversified equity exposure remains the core building block for preserving purchasing power and compounding wealth in real terms over time.

Conclusion

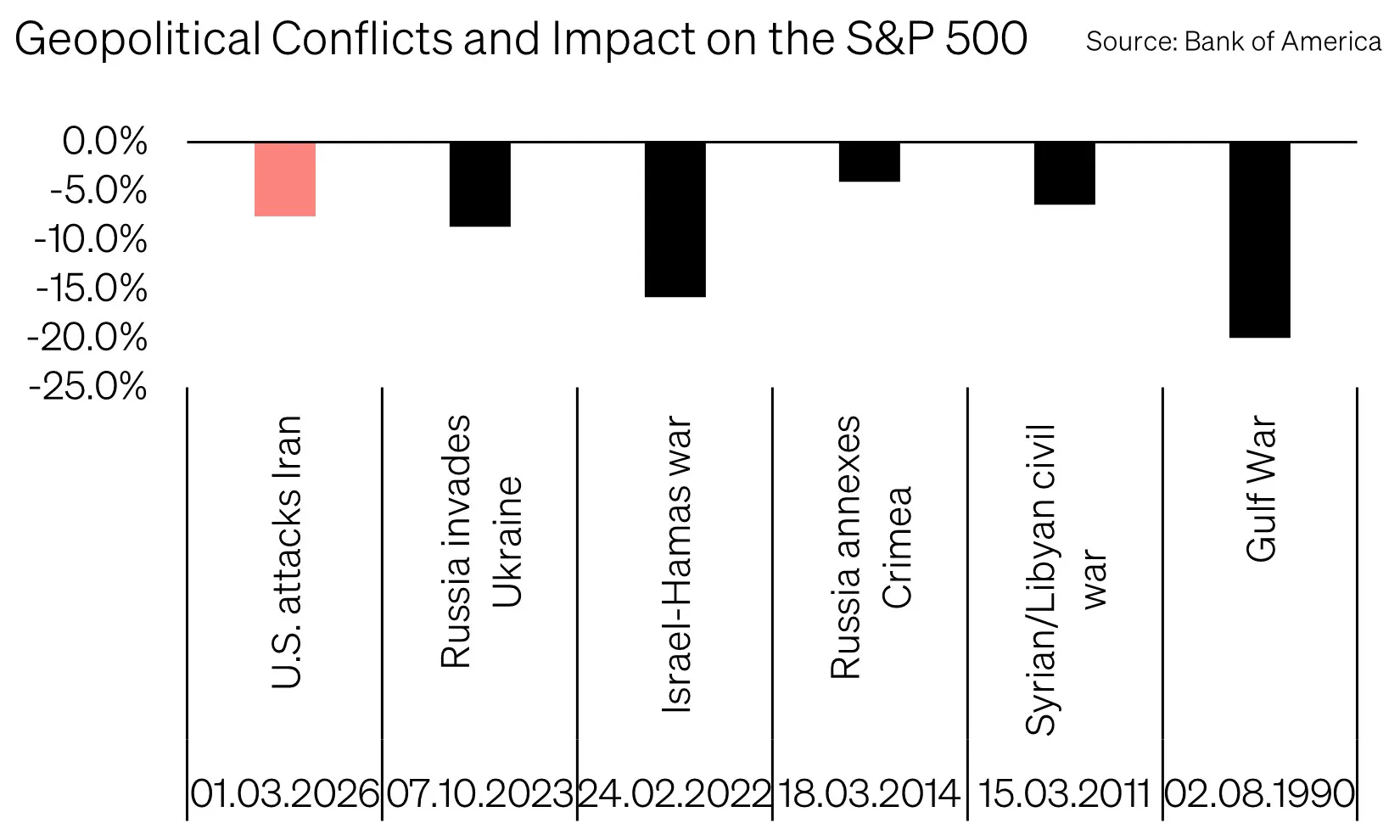

The current market move primarily reflects rising uncertainty—not necessarily a structural break. Historical comparisons show that geopolitical shocks and energy price spikes only rarely trigger lasting market sell-offs. On average, short-term declines in the S&P 500 have amounted to around -5% before markets eventually stabilised.

Inflationary effects from such shocks are also often temporary, provided the disruption does not evolve into a prolonged supply shortage. Over time, adjustment mechanisms typically begin to take effect: alternative energy sources, substitution effects, and monetary as well as fiscal responses can all help cushion the economic fallout.

That said, the current starting point is more demanding than in previous episodes. Valuations across many segments of the market have risen following the constructive macroeconomic developments of recent quarters. This leaves markets more vulnerable to negative surprises and amplifies short-term reactions.

The current volatility should therefore be understood less as a structural risk and more as an adjustment phase within a changed environment. For investors, the key message remains unchanged: discipline, diversification and a long-term perspective are essential—while exaggerated market moves can selectively create attractive opportunities.

Appendix & Disclaimer

Mit SoundInsights beurteilen wir systematisch und konsistent die Aspekte, die für die Entwicklung der Finanzmärkte relevant sind. In der Folge können sich unsere Kunden auf eine rationale und antizyklische Umsetzung unserer Anlageentscheidungen verlassen.

- Konzentration auf das Wesentliche

Zinsniveau, Risikoaufschlag, Bewertung, Wirtschaftsentwicklung, Anlegerstimmung und -positionierung. Das sind die zentralen Faktoren. Sie entscheiden über den Erfolg an den Finanzmärkten. Besonders in turbulenten Zeiten, wenn die Versuchung besonders gross ist, irrational den Schlagzeilen hinterherzulaufen. - Vergleichbarkeit über Ort und Zeit

Die genannten Faktoren sind für alle Märkte und zu jeder Zeit gleichermassen relevant. Dies ergab sich aus einem strengen «Backtesting», welches sich rollend in die Zukunft fortsetzt. - Bündeln unserer kumulierten Anlageerfahrung

Unsere Stärke liegt in den langjährigen Erfahrungen unserer Partner und Principals. Genau diese Erfahrungen fassen wir zusammen und machen sie mittels SoundInsights anwendbar. - Transparenz

Durch die monatliche Publikation wissen unsere Kunden stets, wo wir im Anlagezyklus stehen und wohin die Reise an den Finanzmärkten geht.

Das vorliegende Dokument dient ausschliesslich zu Informationszwecken und ist als Werbung zu verstehen. Es wurde von SoundCapital (nachfolgend «SC») mit grösster Sorgfalt erstellt. Trotz sorgfältiger Bearbeitung übernimmt SC keine Gewähr für die Richtigkeit, Vollständigkeit oder Aktualität der enthaltenen Informationen und lehnt jegliche Haftung für Verluste ab, die durch die Nutzung dieses Dokuments entstehen könnten. Die in diesem Dokument geäusserten Meinungen spiegeln die Einschätzungen von SC zum Zeitpunkt der Erstellung wider und können sich ohne vorherige Ankündigung ändern. Es handelt sich weder um ein Angebot noch eine Empfehlung zum Kauf oder Verkauf von Finanzinstrumenten oder zur Inanspruchnahme von Dienstleistungen. Empfängern wird empfohlen, eigene Beurteilungen vorzunehmen und gegebenenfalls unter Hinzuziehung eines Beraters die Informationen in Bezug auf ihre individuellen Umstände sowie deren rechtliche, regulatorische und steuerliche Auswirkungen zu überprüfen. Obwohl die Informationen aus als zuverlässig angesehenen Quellen stammen, übernimmt SC keine Garantie für deren Genauigkeit. Vergangene Wertentwicklungen von Anlagen sind kein verlässlicher Indikator für zukünftige Ergebnisse. Ebenso sind Prognosen zur Wertentwicklung nicht als verlässlicher Indikator für künftige Ergebnisse zu verstehen. Dieses Dokument richtet sich nicht an Personen, deren Nationalität oder Wohnsitz den Zugang zu solchen Informationen rechtlich einschränkt. Eine Vervielfältigung, auch auszugsweise, ist nur mit ausdrücklicher schriftlicher Genehmigung von SC gestattet.

© 2026 SoundCapital.

Datenquelle: Bloomberg, BofA ML Research