SC — INSIGHTN°47

SoundInsightN°28

01

Germany transitions from austerity to a historic investment offensive.

02

Trump's proposed cuts fundamentally challenge the role of government.

03

Bond markets caught between an inflation and growth dilemma.

Bonds

Overview

Yields

Spreads

UnattractiveAttractive

Equities

Overview

Risk Premium

Leading Indicators

Risk Index

UnattractiveAttractive

Posted 3/26/2025 by Christian Luchsinger

Dual Paradigm Shift in Fiscal Policy

From austerity to activism, from expansionary to restrictive policies. Last months events mark a turning point on both sides of the Atlantic. These fiscal shifts indicate a profound realignment of the state's role. Investors must now navigate an environment increasingly shaped by politics.

Economy

USA: Government as the Problem, Not the Solution

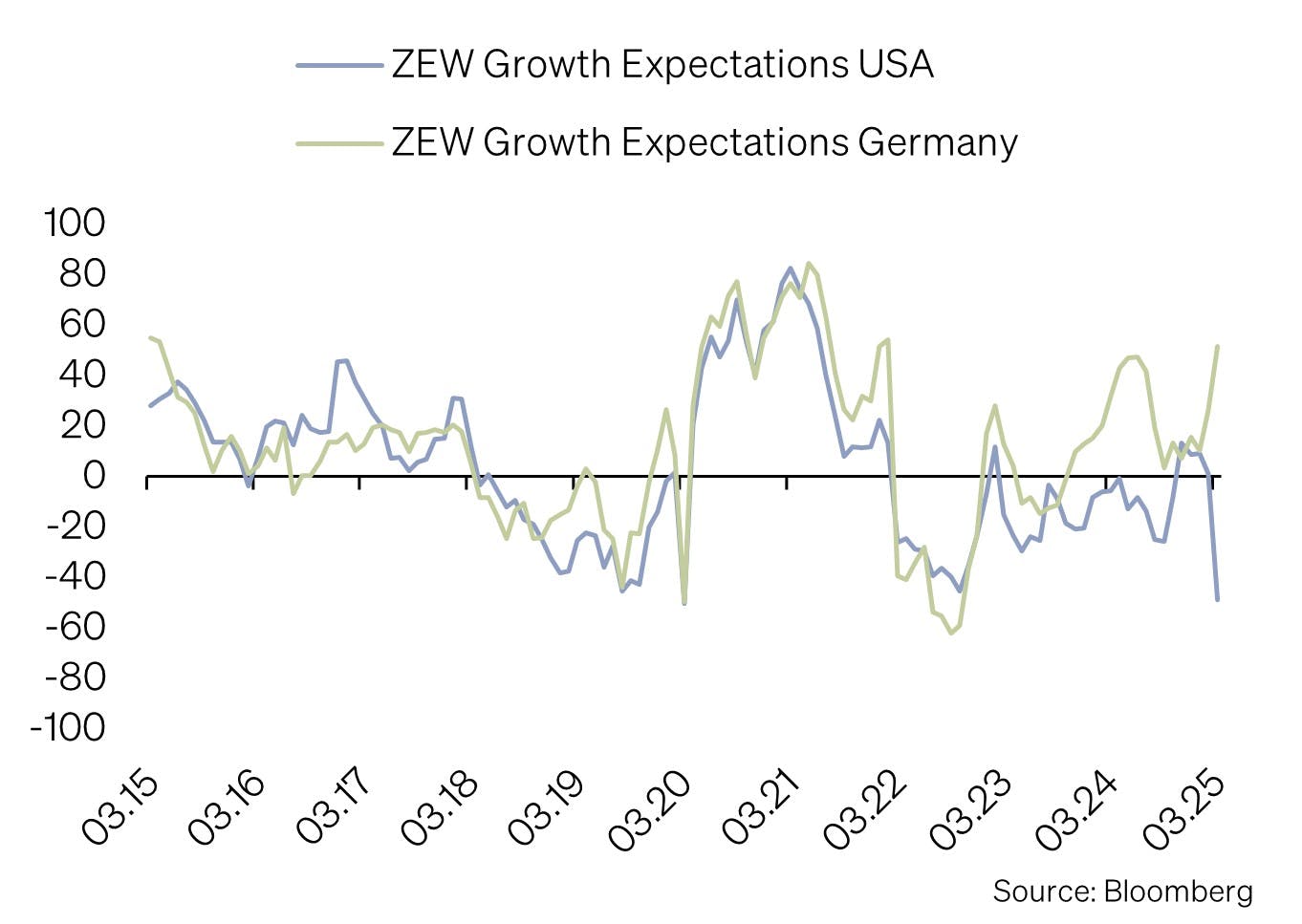

The US fiscal policy is facing a significant directional shift. While the Biden administration focused on substantial governmental investments in infrastructure, climate initiatives, and social programs (such as the Inflation Reduction Act and CHIPS Act), Donald Trump is now advocating a radical downsizing of government functions. His plans include eliminating entire departments like Education, substantial budget cuts to federal agencies such as the Environmental Protection Agency (EPA), and substantial tax cuts for businesses and affluent individuals. In contrast, Biden pursued higher minimum taxes for large corporations, targeted investments in green technology, and strengthened the Internal Revenue Service (IRS) to curb tax avoidance. These competing fiscal visions present substantial implications for both the economy and society.

Germany: From Austerity to Investment

In contrast: Germany is departing from its era of strict fiscal austerity. CDU/CSU and SPD agreed upon a historic €500 billion special fund directed towards defense, infrastructure, education, digitalization, and climate protection. Additionally, Germany’s debt brake is being reformed to permanently exclude defense spending above 1% of GDP. For the first time, federal states will have the capacity to incur deficits specifically for future-oriented investments. UBS expects notable economic stimulus, projecting GDP growth to rise by +0.5 to +0.8 percentage points. This shift marks both a political and economic turning point, effectively ending Europe's era of austerity.

A recent survey by the Centre for European Economic Research highlights substantial changes in economic growth expectations for both countries.

Bond Markets

Global bond markets exhibited mixed performance over the past month, driven largely by these fiscal transitions.

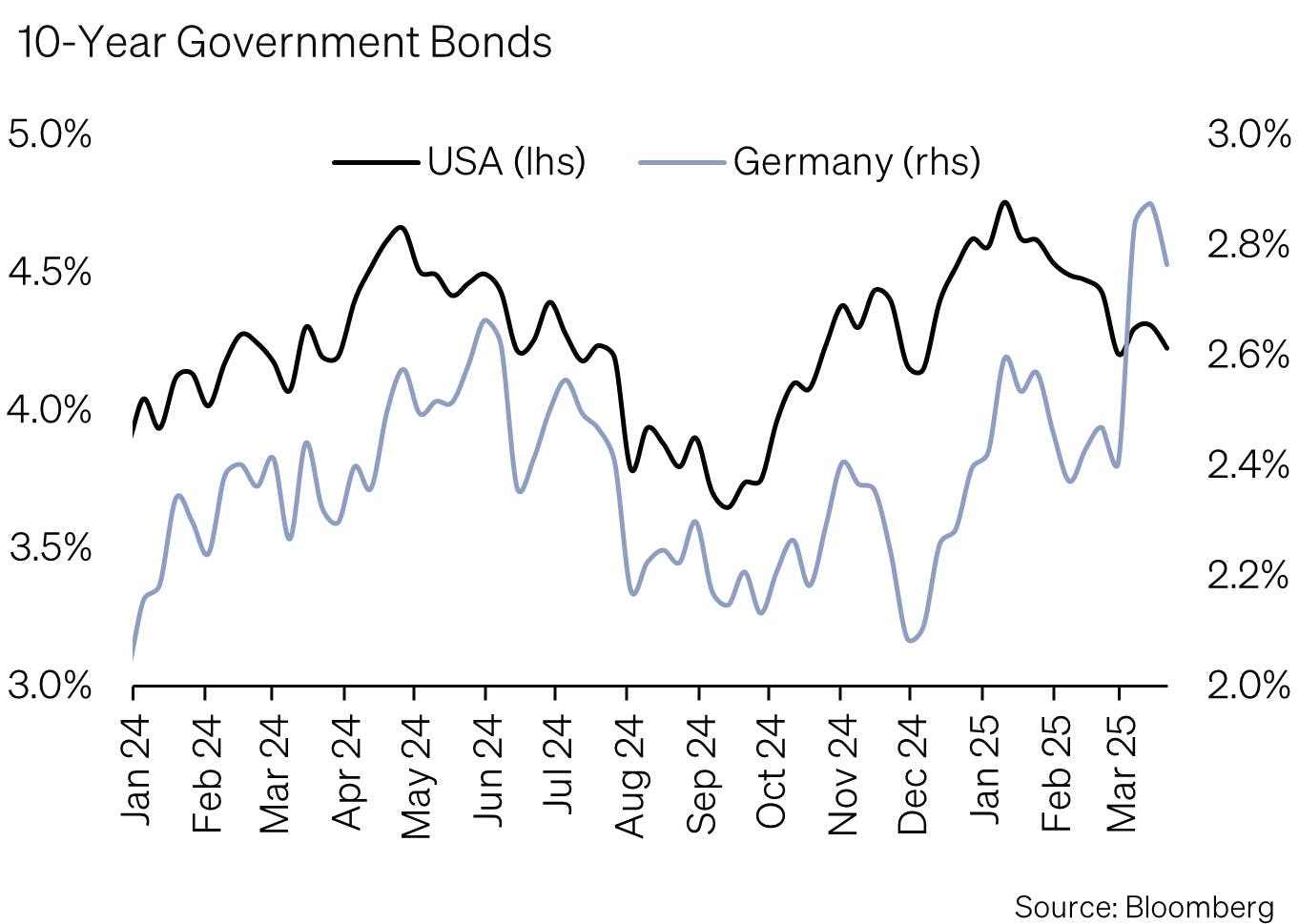

USA: Falling Yields and the Fed’s Dilemma

US treasury yields declined in response to protectionist measures proposed by the Trump administration. New tariffs heightened concerns about increased production costs and potential inflationary risks. The Federal Reserve faces the complex challenge of balancing the risks of economic slowdown with increasing inflationary pressures. The Fed left its key interest rate unchanged, adopting a cautious stance. Fed Chairman Jerome Powell emphasized in a press conference that inflationary impacts from tariff-induced price hikes were temporary, asserting that the US economy remains fundamentally robust.

Europe: Historic Yield Increase in Germany

In Germany, the announced investment package and resulting debt increase have triggered a substantial rise in the yields of ten-year government bonds—the sharpest since the 1990s. Similar, though less pronounced, trends emerged in other Eurozone countries. In contrast, Switzerland reduced its benchmark interest rate further to weaken the Swiss Franc, thereby making CHF bonds increasingly unattractive.

Despite growing concerns about global economic growth, credit spreads barely reacted, indicating overall market stability.

Equity Markets

Europe performed well while the US market corrected sharply

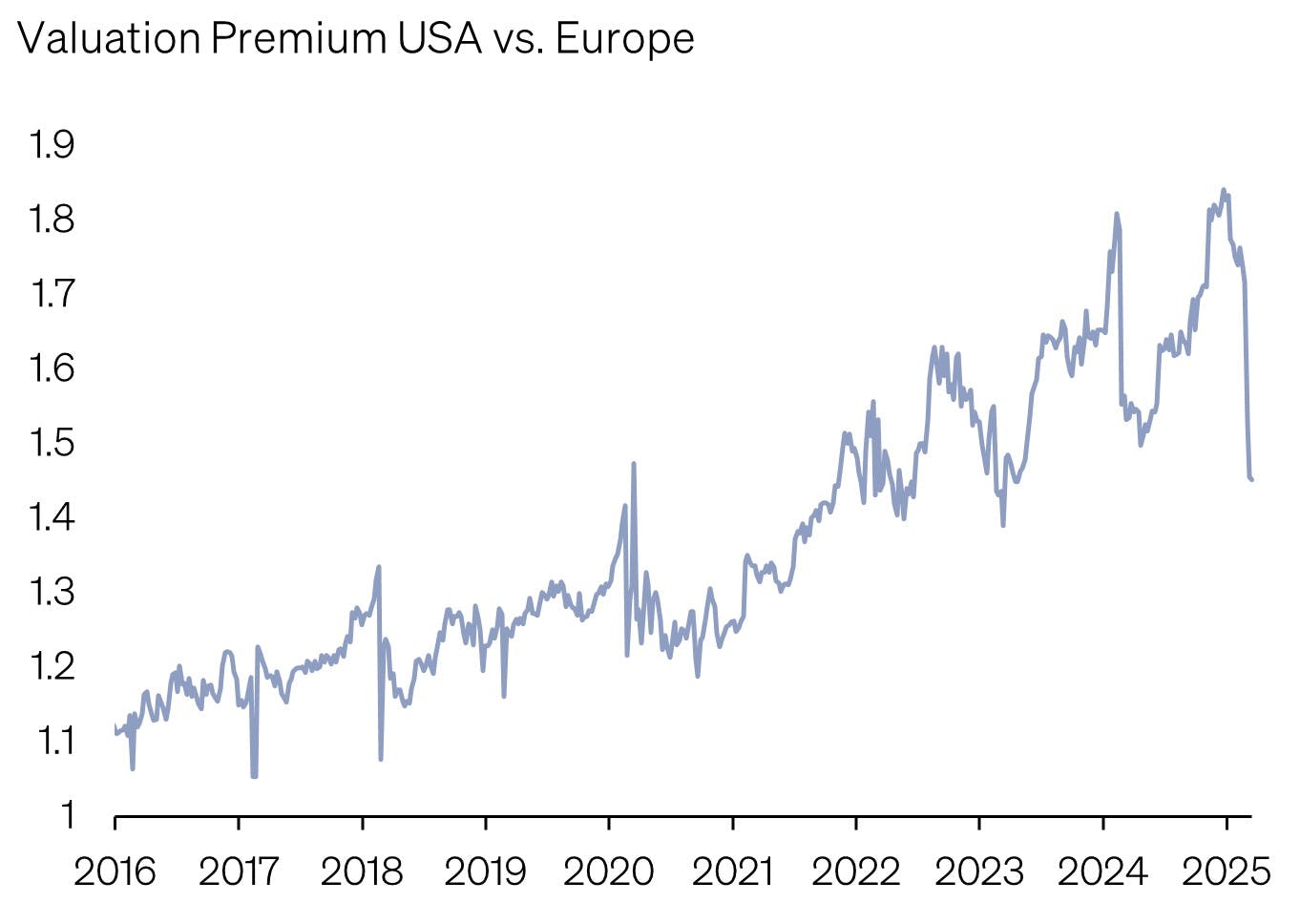

The S&P 500 dropped by 7% year-to-date, impacted by growth concerns and declining valuations in the technology sector. Conversely, European markets benefited from significant capital inflows, driven by favorable valuations and positive fiscal stimuli. Consequently, the Euro STOXX 50 significantly outperformed US indices. Despite this short-term strength, Europe's valuation is still below global markets, currently attracting investor interest.

Recent market movements have notably narrowed the valuation premium (price/earnings ratio) of US stocks compared to Europe, reflecting improved growth expectations for Europe and diminished expectations for the US. However, US economic growth is expected to remain stronger in the short term, continuing to justify a valuation premium.

Market Positioning

Despite substantial market disruptions in March, our proven indicators remain unchanged. The recent correction in equity markets represents a healthy normalization of previously high valuations, particularly in the US.

In our view, artificial intelligence (AI) will be a significant medium-term growth driver, akin to the TMT wave of the 1990s. Investors are advised to maintain a long-term investment perspective to capitalize on AI’s productivity potential, despite interim volatility and market turbulence.

Adjustments to Strategic Allocation

Given the recent interest rate cut by the Swiss National Bank (SNB) and persistently low CHF interest rates, we see limited long-term value in maintaining strategic positions in Swiss government bonds. Consequently, we have reduced our strategic exposure to this asset category in favor of Swiss equities.

Liquidity reduced in favor of alternative investments

Amid declining interest rates coupled with rising inflation, we have reduced our tactical overweight in cash holdings, reallocating capital towards alternative investments.

Adding China Equities

Within emerging market equities, we have increased our allocation to China, though we continue to maintain an overall underweight in emerging markets. This adjustment reflects improved economic conditions, supportive market sentiment, extensive state-led stimulus programs, targeted measures to boost domestic demand and significant advancements in AI technology.

Appendix & Disclaimer

SoundInsights is the central tool for our investment allocation. We use it to systematically and consistently assess the aspects that are relevant to the development of the financial markets. As a result, our clients can rely on a rational and anti-cyclical implementation of our investment decisions.

- Focusing on the essentials

Interest rate level, risk premium, valuation, economic development, investor sentiment and positioning. These are the decisive factors for success on the financial markets, especially in turbulent times when the temptation to react irrationally to the headlines is particularly strong. - Comparability over time and place

The factors mentioned above are equally relevant for all markets and at all times. This is the result of a strict «backtesting» process that continues into the future. - Cumulating our investment experience

Our strength lies in the many years of experience of our partners and principals. It is precisely this experience that we summarize and make it applicable with SoundInsights. - Transparency

Thanks to our monthly publication, our clients always know where we stand in the investment cycle and how we expect the financial markets to develop.

This document is an advertisement and is intended solely for information purposes and for the exclusive use by the recipient. This document was produced by SoundCapital (hereafter «SoundCapital») with the greatest of care and to the best of its knowledge and belief. However, SoundCapital does not warrant any guarantee with regard to its correctness and completeness and does not accept any liability for losses that might occur through the use of this information. This document does not constitute an offer or a recommendation for the purchase or sale of financial instruments or services and does not discharge the recipient from his own judgment. Particularly, it is recommended that the recipient, if needed by consulting professional guidance, assess the information in consideration of his personal situation with regard to legal, regulatory and tax consequences that might be invoked. Although information and data contained in this document originate form sources that are deemed to be reliable, no guarantee is offered regarding the accuracy or completeness. A past performance of an investment does not constitute any guarantee of its performance in the future. Performance forecasts do not serve as a reliable indicator of future results. This document is expressly not intended for persons who, due to their nationality or place of residence, are not permitted access to such information under local law. It may not be reproduced either in part or in full without the written permission of SoundCapital.

© 2025 SoundCapital. All rights reserved.

Datasource: Bloomberg, BofA ML Research