SC — INSIGHTN°48

SoundInsightN°47

01

Iran memorandum raises hopes for relief in oil markets

02

New Fed leadership signals a stronger focus on price stability

03

Low volatility meets rising geopolitical and monetary-policy risks

Bonds

Overview

Interest Rates

Credit Spreads

UnattractiveAttractive

Equities

Overview

-1

Equity Risk Premium

Leading Indicators

Risk Index

-2

UnattractiveAttractive

Posted 6/24/2026 by Christian Luchsinger

Hope, Hype and Reality

Financial markets are currently moving between confidence and caution. A potential agreement between the United States and Iran has temporarily eased pressure on the oil market and raised the prospect of a disinflationary impulse. At the same time, the new leadership of the US Federal Reserve is signalling a stronger focus on price stability and, with it, less willingness to cushion market volatility.

In addition, markets are facing an IPO wave of historic proportions. SpaceX, OpenAI and Anthropic are not only setting new valuation benchmarks; they could also trigger significant capital rotations. For investors, this creates an environment in which opportunities remain available, but market fluctuations are likely to increase.

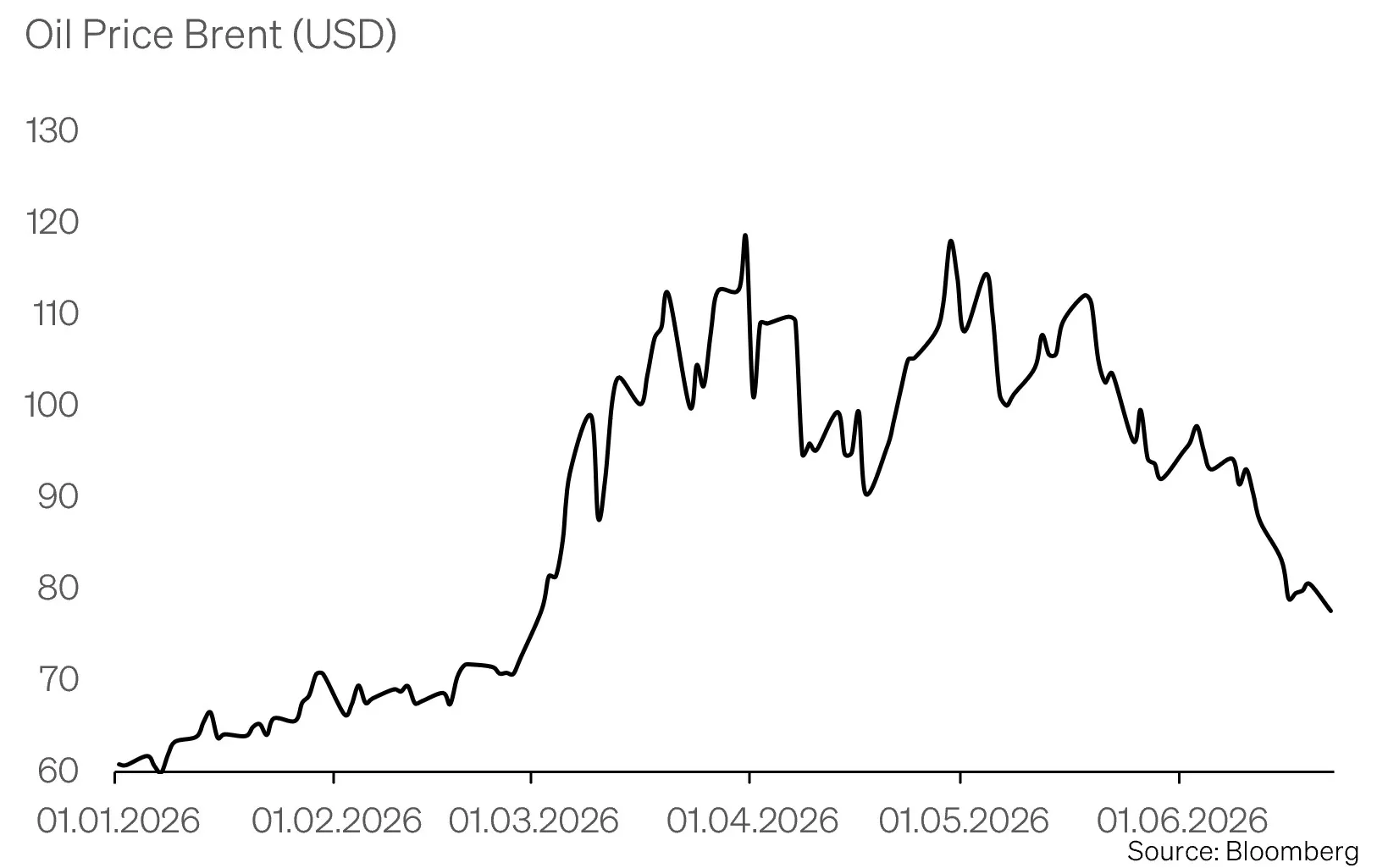

Hope in Iran

The memorandum between the United States and Iran has provided short-term relief for the oil market. The Strait of Hormuz is expected to reopen for commercial shipping. Transit fees are to be temporarily suspended, US waivers will allow Iranian crude oil exports, and some frozen assets are set to be released. In return, Iran has committed to refraining from highly enriched uranium and allowing inspections by the IAEA.

For markets, this initially represents a clear de-escalation. The blockade of Iranian ports has been lifted, the first vessels have returned, and oil prices have declined. At the same time, persistently elevated volatility shows that the geopolitical risk premium has fallen, but not disappeared.

The key question now is implementation. Trade flows do not normalise simply because an agreement has been signed. Shipping companies, insurers and commodity traders need reliable security signals before returning to normal operations. As long as war-risk premiums remain elevated and Iran continues to influence which vessels are considered hostile, passage through the Strait of Hormuz remains operationally vulnerable.

Politically, the memorandum is not yet a final solution either. The tense situation in Lebanon and the fact that Israel is not part of the agreement keep escalation risks elevated. Additional pressure is coming from parts of the Israeli cabinet as well as from US domestic politics, where critics fear a stabilisation of Iran’s nuclear status.

From a macroeconomic perspective, the most important transmission channel remains the price of oil. A more permanently open Strait of Hormuz and additional Iranian exports would be disinflationary, particularly for energy-dependent economies in Europe and Asia. However, this effect will only prove sustainable if physical supply flows, insurance costs and freight rates genuinely normalise.

For investors, the coming days will therefore be critical. The focus will be on IAEA access, the resumption of nuclear talks, Israel’s response, tanker traffic, insurance costs and the question of how OPEC+ reacts to additional Iranian supply.

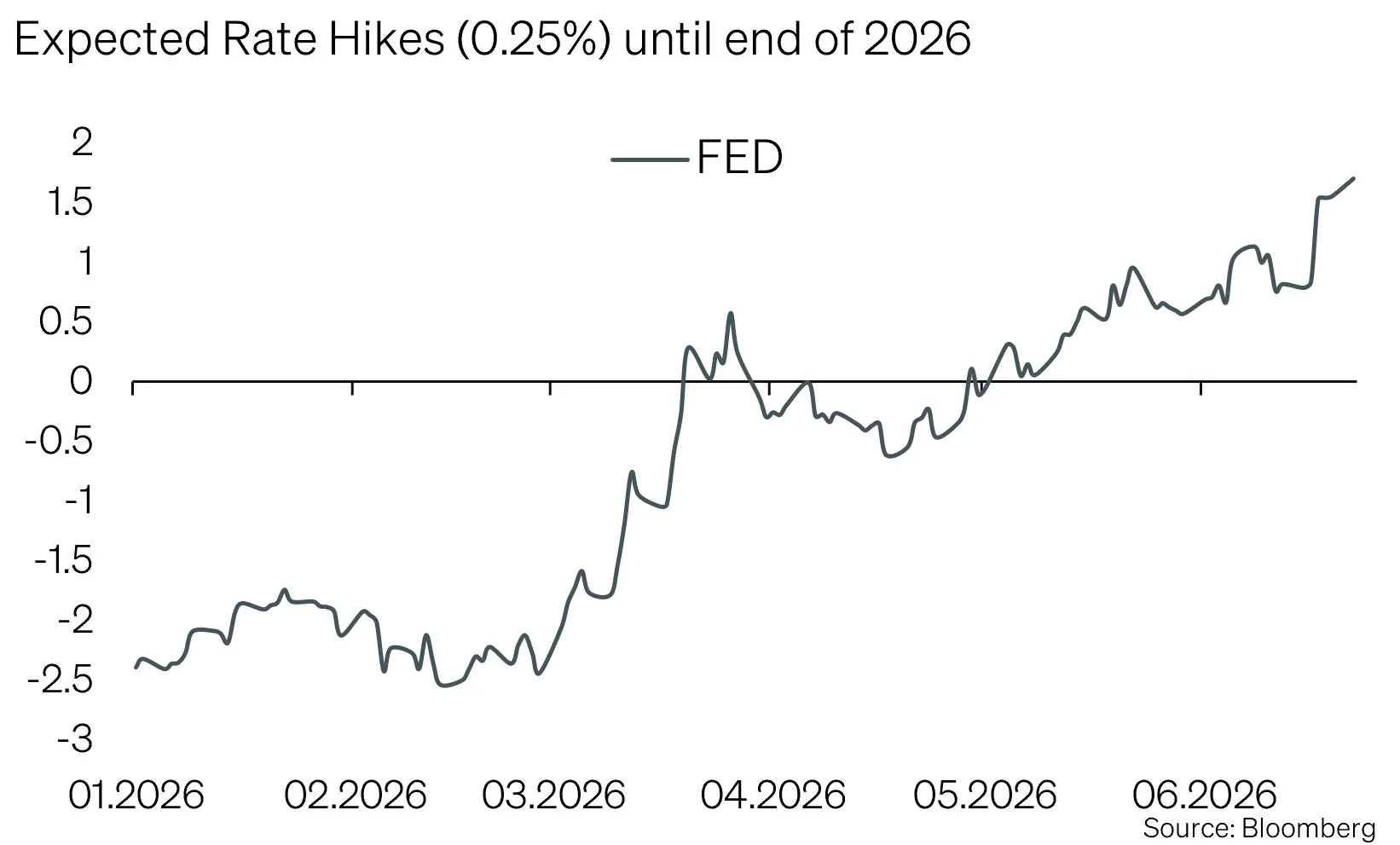

A New Reality in Monetary Policy

The US Federal Reserve left the target range for the federal funds rate unchanged, as expected, at 3.50% to 3.75%. Beneath the surface, however, the meeting marked a clear shift in direction under the new Fed Chair, Kevin Warsh.

The statement was significantly shortened. The dot plot was published without a separate projection from the new Chair, and several working groups are set to review key Fed instruments, including forward guidance, balance-sheet policy and the Summary of Economic Projections. The message is clear: price stability is moving back to the forefront, ahead of communication aimed at calming markets.

Warsh made it clear that high prices for the US population should not be treated as a temporary problem. For investors, less forward guidance also means less planning certainty. The Fed appears willing to accept more market volatility if doing so strengthens its credibility in the fight against inflation.

The new projections underline this shift. The median expectation for the policy rate in 2026 rose to 3.75%, up from 3.375% in March. Rate expectations for 2027 and 2028 were also revised higher. Nine of 18 members now expect at least one rate hike this year, with six of them expecting at least two. At the same time, the growth outlook was revised slightly lower.

This combination is challenging for markets: less tolerance for growth weakness, but a higher bar for a sustained decline in inflation. Bond markets reacted accordingly. The yield on two-year US Treasuries rose sharply, while long-dated yields declined. The resulting bear flattening shows that markets are pricing in more monetary-policy firmness at the short end, but not a stronger long-term growth path.

The US dollar also strengthened. This is relevant for global portfolios, as a stronger dollar can drain liquidity from those market segments that are particularly sensitive to higher US real yields.

The next test will come with the inflation data. If the disinflationary impulse from the Iran memorandum proves strong enough, Warsh can pause in September without losing credibility. If energy prices, producer prices or services inflation remain persistent, however, Bank of America believes the Fed could raise rates as many as three times this year.

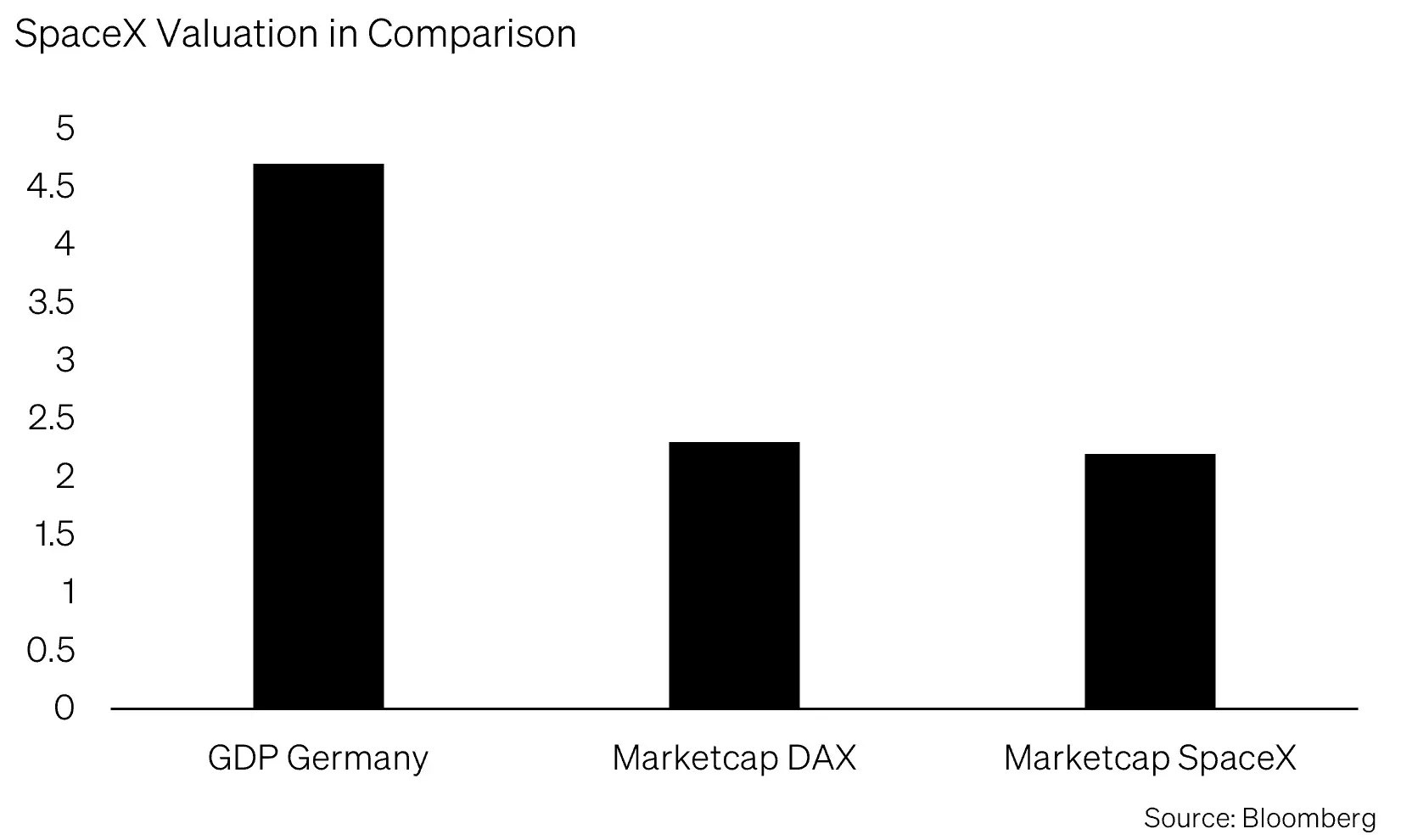

IPO Hype

The IPO of SpaceX marks a new phase for capital markets. The company raised USD 75 billion, significantly surpassing the previous IPO record set by Saudi Aramco.

Its significance goes far beyond SpaceX itself. The IPO shows that public markets are prepared to absorb private-market mega-valuations, provided the growth story is compelling. Starlink, AI infrastructure and the planned acquisition of Cursor provide exactly that narrative.

OpenAI and Anthropic are also potential IPO candidates, with valuations that until recently seemed conceivable mainly in private markets. At the same time, their capital requirements are rising sharply.

Together, SpaceX, OpenAI and Anthropic represent an implied value of around USD 3.6 trillion. An IPO pipeline of this size within a twelve-month period would be historically exceptional. The market would not only have to absorb new shares, but also reprice index weights, passive inflows and valuation anchors. Once such companies are included in major indices, passive funds become structural buyers. At the same time, this can trigger capital rotations out of existing holdings.

The comparison with the dot-com era and the growth wave of 2021 is obvious, but incomplete. As in those periods, high valuations are meeting the promise of structural disruption. Unlike many companies from those earlier phases, however, SpaceX, OpenAI and Anthropic have real revenues, strategic relevance and technological differentiation. This reduces the risk of pure hype, but does not eliminate it.

The decisive difference lies in the interest-rate environment. Higher rates for longer are particularly challenging for companies whose valuations depend heavily on future cash flows and whose investment needs are immediate. This is precisely why Fed policy is so important for this IPO wave.

For private markets, this IPO wave represents an important release valve. Venture-capital and crossover investors could finally obtain liquidity from positions that have been tied up in private portfolios for years. Part of this capital is likely to flow back into the next generation of AI companies. The wave could therefore relieve pressure while also creating new signs of overheating.

SoundCapital Positioning

We are maintaining our overall investment stance, while making portfolios tactically more robust. The long-term growth themes remain intact. At the same time, recent market developments have increased the risk of short-term setbacks: residual geopolitical uncertainty, a less market-friendly Fed, tight credit spreads and potential valuation excesses in the AI segment are all coinciding with low volatility levels. Against this backdrop, we have implemented an equity hedge.

This hedge does not represent a move away from risk assets. Rather, it is designed to combine participation in structural opportunities with more deliberate risk management. We remain invested, but are reducing vulnerability to abrupt market moves.

Bonds

Within fixed income, we remain overweight high-quality corporate bonds. Persistently tight credit spreads confirm our cautious stance towards high-yield bonds. In our view, investors are currently receiving only limited compensation for taking on additional credit risk.

Equities

Our regional overweight in emerging markets remains in place. Valuations, positioning and structural growth continue to support the region. The global value creation of the AI boom also confirms that important parts of the supply chain lie outside the United States and can benefit from this investment cycle.

We have hedged a part of the equity allocation because of the increasingly euphoric market positioning. The hedge is intended to cushion potential setbacks without abandoning strategic exposure to long-term growth themes. In an environment where central-bank policy, geopolitics and valuation questions are becoming more closely intertwined, such a risk buffer appears appropriate.

Alternative Investments

Gold retains its role as a diversifier in an environment of heightened political and monetary-policy uncertainty. The prospect of higher interest rates has recently weighed on the gold price, but it does not change the long-term structural case for the precious metal.

Conclusion

The three themes of hope, hype and reality are more closely connected than they may appear at first glance. Through lower oil prices and normalised transport costs, the Iran memorandum offers hope for a disinflationary impulse. This impulse would be important for markets precisely because the Fed under Kevin Warsh has clearly signalled that it is more focused on inflation and credibility than on stabilising short-term market sentiment.

This makes the market environment more sensitive. If energy prices fall sustainably, interest rates are likely to remain around current levels. If oil prices, producer prices or services inflation remain persistent, however, the Fed is likely to respond more quickly and more decisively than before. For risk assets, this means that positive growth and technology themes must be weighed more carefully against higher discount rates and a less market-friendly monetary policy.

This is the environment into which a potentially historic AI IPO wave is now emerging. The largest public listings in history could release new liquidity, but they could also intensify valuation questions, index rotations and supply pressure. Precisely because the structural importance of AI is undisputed, the price investors pay for that exposure becomes all the more important.

For portfolios, this does not argue against risk assets, but it does call for greater selectivity and more deliberate risk management. When geopolitical easing, an inflation-focused Fed and historic IPO volumes converge, market nervousness is more likely to rise than fall. In an environment of low volatility, hedging therefore appears attractive: as a complement to positioning, not as a substitute for it.

Appendix & Disclaimer

Mit SoundInsights beurteilen wir systematisch und konsistent die Aspekte, die für die Entwicklung der Finanzmärkte relevant sind. In der Folge können sich unsere Kunden auf eine rationale und antizyklische Umsetzung unserer Anlageentscheidungen verlassen.

- Konzentration auf das Wesentliche

Zinsniveau, Risikoaufschlag, Bewertung, Wirtschaftsentwicklung, Anlegerstimmung und -positionierung. Das sind die zentralen Faktoren. Sie entscheiden über den Erfolg an den Finanzmärkten. Besonders in turbulenten Zeiten, wenn die Versuchung besonders gross ist, irrational den Schlagzeilen hinterherzulaufen. - Vergleichbarkeit über Ort und Zeit

Die genannten Faktoren sind für alle Märkte und zu jeder Zeit gleichermassen relevant. Dies ergab sich aus einem strengen «Backtesting», welches sich rollend in die Zukunft fortsetzt. - Bündeln unserer kumulierten Anlageerfahrung

Unsere Stärke liegt in den langjährigen Erfahrungen unserer Partner und Principals. Genau diese Erfahrungen fassen wir zusammen und machen sie mittels SoundInsights anwendbar. - Transparenz

Durch die monatliche Publikation wissen unsere Kunden stets, wo wir im Anlagezyklus stehen und wohin die Reise an den Finanzmärkten geht.

Das vorliegende Dokument dient ausschliesslich zu Informationszwecken und ist als Werbung zu verstehen. Es wurde von SoundCapital (nachfolgend «SC») mit grösster Sorgfalt erstellt. Trotz sorgfältiger Bearbeitung übernimmt SC keine Gewähr für die Richtigkeit, Vollständigkeit oder Aktualität der enthaltenen Informationen und lehnt jegliche Haftung für Verluste ab, die durch die Nutzung dieses Dokuments entstehen könnten. Die in diesem Dokument geäusserten Meinungen spiegeln die Einschätzungen von SC zum Zeitpunkt der Erstellung wider und können sich ohne vorherige Ankündigung ändern. Es handelt sich weder um ein Angebot noch eine Empfehlung zum Kauf oder Verkauf von Finanzinstrumenten oder zur Inanspruchnahme von Dienstleistungen. Empfängern wird empfohlen, eigene Beurteilungen vorzunehmen und gegebenenfalls unter Hinzuziehung eines Beraters die Informationen in Bezug auf ihre individuellen Umstände sowie deren rechtliche, regulatorische und steuerliche Auswirkungen zu überprüfen. Obwohl die Informationen aus als zuverlässig angesehenen Quellen stammen, übernimmt SC keine Garantie für deren Genauigkeit. Vergangene Wertentwicklungen von Anlagen sind kein verlässlicher Indikator für zukünftige Ergebnisse. Ebenso sind Prognosen zur Wertentwicklung nicht als verlässlicher Indikator für künftige Ergebnisse zu verstehen. Dieses Dokument richtet sich nicht an Personen, deren Nationalität oder Wohnsitz den Zugang zu solchen Informationen rechtlich einschränkt. Eine Vervielfältigung, auch auszugsweise, ist nur mit ausdrücklicher schriftlicher Genehmigung von SC gestattet.

© 2026 SoundCapital.

Datenquelle: Bloomberg, BofA ML Research